Four Dissents, $126 Oil, and 3.2% Inflation: What the Week Ending May 1 Means for Gold and Your Portfolio

WiseGold Weekly Pulse | May 1, 2026

Coverage Period: April 24, 2026 (00:00:00 EST) to May 1, 2026 (11:00:00 EST)

WiseGold Capital partners with advisors to assist them in managing assets for their clients. WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Nothing in this publication constitutes investment advice.

Executive Summary

The week ending May 1, 2026, was characterized by a confluence of hawkish central bank holds, persistent inflation data, and elevated geopolitical risk premiums stemming from the ongoing Middle East conflict. The Federal Reserve maintained its benchmark rate at 3.50%-3.75%, though a notable four dissents underscored internal divisions regarding the policy path [1]. Meanwhile, the European Central Bank (ECB) and Bank of Japan (BoJ) also held rates steady, with the ECB signaling a potential June hike and the BoJ halving its growth forecast [2] [3]. U.S. economic data presented a mixed picture: Q1 GDP advanced at a 2.0% annualized rate, reflecting solid but moderating growth, while the Core PCE price index climbed 3.2% year-over-year, reinforcing the “higher-for-longer” narrative [4] [5]. Energy markets remained a focal point, with Brent crude surging to a wartime high of $126/bbl amid disruptions in the Strait of Hormuz, before retreating slightly [6]. In the precious metals complex, gold and silver experienced volatile trading, ultimately finding support from safe-haven demand and central bank accumulation, despite headwinds from a resilient U.S. dollar and elevated Treasury yields [7] [8].

Key Takeaways:

- Fed Holds Steady: The FOMC maintained rates at 3.50%-3.75%, with four dissents highlighting policy uncertainty [1].

- Inflation Persists: U.S. Core PCE rose 3.2% YoY, complicating the timeline for potential rate cuts [5].

- Energy Shock: Brent crude spiked to $126/bbl amid Middle East tensions, driving inflation fears [6].

- Metals Resilience: Gold and silver found support from safe-haven flows and robust central bank buying [7] [8].

- Yields Elevated: The 10-year U.S. Treasury yield hovered around 4.40%, reflecting the hawkish policy outlook [9].

Market & Macro Week-in-Review Timeline

- Fri Apr 24: U.S. natural gas futures fall to $2.52/MMBtu, a level last seen in late 2024 [10].

- Mon Apr 27: Markets balance risk appetite against renewed geopolitical strain as U.S.-Iran peace talks stall [11].

- Tue Apr 28: The UAE announces its exit from OPEC, dealing a blow to the oil producers’ group [12].

- Wed Apr 29: The Federal Reserve holds rates at 3.50%-3.75% with four dissents; Chair Powell emphasizes data dependence [1].

- Thu Apr 30: U.S. Q1 GDP advance estimate shows 2.0% annualized growth; Core PCE inflation hits 3.2% [4] [5]. The ECB holds rates unchanged but debates a June hike [2].

- Fri May 1: (10:00) ISM Manufacturing PMI prints at 52.7, indicating continued sector expansion [13]. Yen jumps as Japan threatens further currency intervention [14].

Thematic Deep Dives

Macro & Monetary Policy

Central banks dominated the week’s narrative, uniformly opting to hold interest rates steady while grappling with persistent inflation and geopolitical uncertainties.

- The Federal Reserve maintained the federal funds rate at 3.50%-3.75%, but the decision was marked by four dissents, signaling a divided committee [1].

- The ECB kept its key rates unchanged but extensively debated a potential hike in June to combat inflation [2].

- The Bank of Japan held rates at 0.75% and halved its growth forecast, while warning of significantly higher inflation [3].

- The Bank of England left rates on hold at 3.75% in an 8–1 split vote, warning of potential future hikes [15].

The synchronized pause across major central banks underscores a cautious approach as policymakers assess the delayed impact of previous tightening and the inflationary pressures arising from the Middle East conflict. The notable dissents within the Fed highlight the growing tension between managing inflation and supporting economic growth.

Inflation & Growth Data

U.S. economic data released this week painted a picture of resilient but moderating growth coupled with stubborn inflation.

- U.S. Q1 GDP (advance estimate) increased at a 2.0% annualized rate, driven by investment, exports, and consumer spending [4].

- The Core PCE price index, the Fed’s preferred inflation gauge, climbed 3.2% year-over-year in March [5].

- The ISM Manufacturing PMI for April registered 52.7, indicating ongoing expansion in the sector [13].

- Eurozone inflation jumped to 3% in April, while Q1 GDP expanded by a meager 0.1% [16].

The combination of 2.0% GDP growth and 3.2% Core PCE inflation in the U.S. reinforces the “higher-for-longer” interest rate narrative. The data suggests that while the economy is avoiding a recession, inflationary pressures remain entrenched, particularly in the services sector, complicating the Fed’s policy path.

Rates & Yield Curve Dynamics

Treasury yields remained elevated throughout the week, reflecting the hawkish central bank holds and persistent inflation data.

- The 10-year U.S. Treasury yield traded around 4.40%, maintaining its recent highs [9].

- The 10Y-2Y Treasury spread stood at 52 basis points, indicating ongoing yield curve inversion [9].

- Mortgage rates remained elevated, with the 30-year fixed rate averaging around 6.40% [17].

The sustained elevation in Treasury yields underscores the market’s repricing of interest rate expectations. The persistent yield curve inversion continues to signal underlying economic concerns, although the resilient GDP data has somewhat mitigated immediate recession fears.

FX & Dollar Landscape

The U.S. dollar exhibited strength against major peers, supported by the hawkish Fed hold and safe-haven demand, while the Japanese yen experienced significant volatility.

- The U.S. Dollar Index (DXY) held firm, trading in the 98.4 to 98.9 range and closing near 98.85 on April 30 [9].

- The Japanese yen jumped against the dollar following threats of further currency intervention by Japanese authorities [14].

- The euro remained relatively stable following the ECB’s rate decision [18].

The dollar’s resilience reflects its dual role as a high-yielding currency in the current interest rate environment and a safe-haven asset amid geopolitical turmoil. The volatility in the yen highlights the challenges faced by the BoJ in managing its currency amidst divergent global monetary policies.

Energy & Broader Commodities Context

Energy markets were highly volatile, driven by the escalating conflict in the Middle East and supply disruptions.

- Brent crude surged to a wartime high of $126/bbl before retreating to close around $111 to $112/bbl on April 30 [6].

- The World Bank projected a 24% surge in energy prices this year due to the Middle East conflict [19].

- The UAE announced its exit from OPEC, potentially reshaping global oil market dynamics [12].

- U.S. natural gas futures climbed as output fell and LNG exports surged [20].

The spike in oil prices underscores the significant geopolitical risk premium currently priced into energy markets. The closure of the Strait of Hormuz and the broader Middle East conflict pose a substantial threat to global energy supplies, with the potential to exacerbate inflationary pressures worldwide.

Precious Metals Focus

Precious metals experienced volatile trading, balancing headwinds from a strong dollar and elevated yields against tailwinds from safe-haven demand and central bank accumulation.

- Gold: Traded roughly $4,567-$4,642/oz during the period, closing near $4,592/oz [21].

- Silver: Traded roughly $72.84-$76.23/oz, closing near $74.46/oz [21] [22].

- Platinum: Surged 5.72% to reclaim the $2,000 handle, closing near $2,003/oz [22].

- Palladium: Added 5.24% to close at $1,556/oz [22].

- Positioning: The World Gold Council reported Q1 central bank gold demand of 244t, up 17% q/q [8]. Physically-backed gold ETF holdings increased by 62t in Q1 [8].

The robust central bank demand and positive ETF flows in Q1 highlight the enduring appeal of gold as a strategic reserve asset and safe-haven investment. The strong performance of platinum and palladium was driven by sector-specific supply concerns and short-covering activity [22].

Credit & Liquidity

Credit markets showed signs of tightening, reflecting the broader macroeconomic uncertainty and elevated interest rates.

- Credit spreads widened, with the CCC spread reaching 8.65% [23].

- The ECB reported a tightening of credit standards for loans to firms in the first quarter [2].

The widening of credit spreads and tightening of lending standards indicate growing caution among lenders and investors. This trend could constrain corporate investment and economic growth in the medium term.

Equity & Volatility Sentiment

Equity markets exhibited resilience despite the hawkish central bank tone and geopolitical risks, while volatility remained relatively subdued.

- The S&P 500 gained 10.4% in April, its best monthly performance since November 2020 [24].

- The CBOE Volatility Index (VIX) fell to the 16 level as risk-on sentiment returned [25].

The strong performance of equity markets suggests that investors are currently prioritizing resilient economic growth and corporate earnings over the risks posed by elevated interest rates and geopolitical tensions. However, the disconnect between equity market exuberance and underlying macroeconomic pressures remains a point of concern.

Geopolitics & Strategic Risk

The ongoing conflict in the Middle East remained the primary source of geopolitical risk, with significant implications for global markets.

- The U.S.-Iran ceasefire that began in early April was reported as “terminated” [26].

- The closure of the Strait of Hormuz continued to disrupt global shipping and energy supplies [19].

The escalation of hostilities in the Middle East poses a severe threat to global economic stability. The potential for further supply chain disruptions and energy price spikes remains a key risk factor for inflation and growth outlooks.

Structural & Long-Term Themes

The week’s events highlighted several structural themes shaping the long-term investment landscape.

- De-dollarization: The continued robust gold buying by central banks, particularly in emerging markets, underscores the ongoing trend of diversifying reserves away from the U.S. dollar [8].

- Energy Transition: The volatility in fossil fuel markets reinforces the strategic imperative of transitioning to renewable energy sources, although near-term reliance on traditional energy remains high.

These structural shifts have profound implications for asset allocation and risk management, emphasizing the need for diversified portfolios that can withstand geopolitical shocks and evolving global economic paradigms.

Cross-Asset Interlinkages

- Hawkish Fed & Strong Dollar: The Fed’s decision to hold rates, coupled with persistent inflation data, supported the U.S. dollar, creating headwinds for dollar-denominated commodities.

- Geopolitics & Energy Prices: The escalation of the Middle East conflict drove Brent crude to wartime highs, directly impacting inflation expectations and reinforcing the “higher-for-longer” interest rate narrative.

- Inflation & Precious Metals: The combination of elevated inflation and geopolitical uncertainty sustained safe-haven demand for gold and silver, counteracting the negative impact of high Treasury yields.

- Supply Disruptions & PGMs: Sector-specific supply concerns in Russia and South Africa drove significant gains in platinum and palladium, decoupling them somewhat from broader macroeconomic trends.

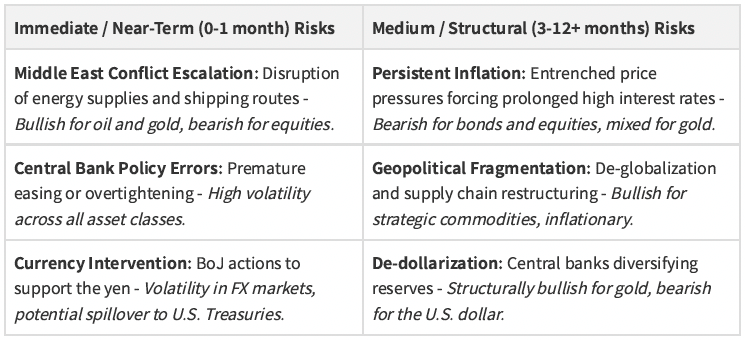

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

- U.S. Nonfarm Payrolls (May 8): A stronger-than-expected jobs report would reinforce the Fed’s hawkish stance. Probability: Base. Precious Metals Sensitivity: Hawkish surprise = potential headwind to bullion.

- Middle East Ceasefire: A sudden de-escalation of hostilities would reduce the geopolitical risk premium. Probability: Low-Probability Tail. Precious Metals Sensitivity: Bearish for gold and oil.

- ECB Rate Hike (June): The ECB following through on its signals to hike rates in June. Probability: Elevated. Precious Metals Sensitivity: Bearish for gold as it signals continued global tightening.

Portfolio Context & Implications

The current macroeconomic environment, characterized by persistent inflation, elevated interest rates, and significant geopolitical risks, underscores the importance of strategic diversification. The resilience of gold and silver in the face of a strong dollar and high yields highlights their utility as non-correlated assets capable of providing portfolio stability during periods of market stress. The structural shift towards de-dollarization and the ongoing accumulation of gold by central banks further reinforce the long-term strategic case for precious metals within a diversified portfolio framework.

Precious Metals Strategic Thesis

Diversification Attribute

Precious metals continue to demonstrate their value as effective portfolio diversifiers, exhibiting low correlation to traditional equities and fixed income, particularly during periods of macroeconomic uncertainty and geopolitical stress.

Wealth Protection & Purchasing Power

In an environment of persistent inflation and fiat currency debasement, gold and silver serve as reliable stores of value, protecting purchasing power over the long term.

Drawdown Mitigation & Crisis Optionality

The safe-haven appeal of precious metals provides crucial drawdown mitigation during market corrections and systemic crises, offering investors valuable optionality when traditional assets falter.

Structural Demand Drivers

Robust central bank accumulation, growing retail demand in emerging markets, and increasing industrial applications for silver and PGMs provide strong structural support for precious metals prices.

Allocation Framing

Historical and academic analysis suggests that a strategic allocation to precious metals can enhance risk-adjusted returns and improve overall portfolio resilience across various economic cycles.

Summary Capsule

- Macro Pulse: Resilient U.S. growth (Q1 GDP +2.0%) paired with sticky inflation (Core PCE +3.2%) reinforces the “higher-for-longer” interest rate regime.

- Metals Stance: Gold and silver remain supported by safe-haven flows and central bank buying, despite headwinds from a strong dollar and elevated yields.

- Risk Tone: Geopolitical tensions in the Middle East are driving significant risk premiums in energy markets, while equity markets exhibit complacency.

- Positioning Nuance: Central banks added 244t of gold to reserves in Q1, underscoring the structural shift towards de-dollarization.

- Forward Watch: Upcoming U.S. labor market data and developments in the Middle East conflict will be key catalysts for near-term market direction.

- Structural Theme: The intersection of geopolitical fragmentation, persistent inflation, and energy transition continues to favor strategic allocations to real assets.

Source List

[1] CNBC — Fed interest rate decision April 2026: Fed holds rates steady amid dissent — April 29, 2026 — https://www.cnbc.com/2026/04/29/fed-interest-rate-decision-april-2026.html [2] European Central Bank — Monetary policy decisions — April 30, 2026 — https://www.ecb.europa.eu/press/pr/date/2026/html/ecb.mp260430~81b7179e6f.en.html [3] Central Banking — BoJ holds rates and halves growth forecast — April 28, 2026 — https://www.centralbanking.com/central-banks/monetary-policy/monetary-policy-decisions/7975698/boj-holds-rates-and-halves-growth-forecast [4] Bureau of Economic Analysis — GDP (Advance Estimate), 1st Quarter 2026 — April 30, 2026 — https://www.bea.gov/news/2026/gdp-advance-estimate-1st-quarter-2026 [5] Advisor Perspectives — Core PCE Inflation at 3.2% in March, Highest Level Since 2023 — April 30, 2026 — https://www.advisorperspectives.com/dshort/updates/2026/04/30/core-pce-inflation-at-3-2-in-march-highest-level-since-2023 [6] CNBC — Brent oil falls after surging to wartime high — April 30, 2026 — https://www.cnbc.com/2026/04/30/oil-prices-today-brent-wti-us-iran-war-trump.html [7] Kitco News — Solid price gains for gold, silver as USDX solidly down — April 30, 2026 — https://www.kitco.com/news/article/2026-04-30/solid-price-gains-gold-silver-usdx-solidly-down [8] World Gold Council — Record gold prices continue to shift demand dynamics — April 29, 2026 — https://www.gold.org/news-and-events/press-releases/record-gold-prices-continue-shift-demand-dynamics [9] AhaSignals — DXY April 2026 Recap: Dollar Index, 10Y Yield & DCDI — April 30, 2026 — https://ahasignals.com/dxy-forecast-april-2026/ [10] American Gas Association — Natural Gas Market Indicators — April 30, 2026 — https://www.aga.org/research-policy/resource-library/natural-gas-market-indicators-april-30-2026/ [11] CNBC — U.S.-Iran peace talks stall. What’s next for global markets — April 27, 2026 — https://www.cnbc.com/2026/04/27/us-iran-peace-talks-stall-global-markets-stocks-oil-treasurys.html [12] Reuters — UAE leaves OPEC in blow to global oil producers’ group — April 28, 2026 — https://www.reuters.com/markets/commodities/uae-says-it-quits-opec-opec-statement-2026-04-28/ [13] PR Newswire — Manufacturing PMI® at 52.7%; April 2026 ISM® — May 1, 2026 — https://www.prnewswire.com/news-releases/manufacturing-pmi-at-52-7-april-2026-ism-manufacturing-pmi-report-302759226.html [14] Reuters — Yen jumps as Japan threatens more intervention — May 1, 2026 — https://www.reuters.com/world/asia-pacific/yen-trims-gains-against-dollar-after-japans-intervention-markets-2026-05-01/ [15] The Guardian — Bank of England leaves interest rates on hold with committee split 8–1 — April 30, 2026 — https://www.theguardian.com/business/live/2026/apr/30/bank-of-england-expected-hold-interest-rates-noon-assesses-fallout-iran-war-live-updates [16] CNBC — Euro zone inflation jumps to 3% as economic growth slows — April 30, 2026 — https://www.cnbc.com/2026/04/30/euro-zone-economy-inflation-growth.html [17] Wall Street Journal — Today’s Mortgage Rates, April 28, 2026: 30-Year — April 28, 2026 — https://www.wsj.com/buyside/personal-finance/mortgage/mortgage-rates-today-4-28-2026 [18] Wall Street Journal — ECB Decision Likely Had Little Impact on Euro — April 30, 2026 — https://www.wsj.com/finance/currencies/yen-likely-to-stay-weak-despite-likely-govt-intervention-62c1023e [19] World Bank — Middle East War to Spark Biggest Energy Price Surge in Four Years — April 28, 2026 — https://www.worldbank.org/en/news/press-release/2026/04/28/commodity-markets-outlook-april-2026-press-release [20] Reuters — US natural gas futures climb as output falls and LNG exports surge — May 1, 2026 — https://www.reuters.com/business/energy/us-natural-gas-futures-climb-output-falls-lng-exports-surge-2026-05-01/ [21] Fortune — Current price of gold: May 1, 2026 — May 1, 2026 — https://fortune.com/article/current-price-of-gold-05-01-2026/ [22] Texas Precious Metals — Precious Metals Market Update: 4/30/2026 — April 30, 2026 — https://texmetals.com/all-news/precious-metals-market-update-4-30-2026 [23] UGC Charts — Credit Spread, VIX and SP500 — April 29, 2026 — https://en.macromicro.me/charts/82929/Credit-Spread-VIX-and-SP500 [24] Barron’s — Markets Enjoyed an Historic April. Why the S&P 500 Could Keep Rising. — May 1, 2026 — https://www.barrons.com/articles/things-to-know-today-ca07d135 [25] AOL — The CBOE VIX Falls to 16 Level as Risk-On Trade Returns — May 1, 2026 — https://www.aol.com/articles/cboe-vix-falls-16-level-142307104.html [26] Reuters — US official says Iran war truce ‘terminated’ hostilities for war powers purposes — May 1, 2026 — https://www.reuters.com/world/middle-east/war-powers-resolution-purposes-us-hostilities-with-iran-that-began-february-have-2026-05-01/

Methodology & Notes

Data compilation approach relies on publicly available, credible financial news and institutional reports published within the coverage window. Price ranges are approximated based on spot and front-month futures data observed during the period. Timestamp conventions are in EST. The report includes Friday 10:00 AM EST data releases where available and relevant.

Disclosure

This report is for informational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instrument. The views expressed are based on publicly available information believed to be reliable, but accuracy or completeness cannot be guaranteed. Past performance is not indicative of future results. Readers should conduct their own analysis and consult qualified professionals before making any financial decisions.

#WiseGold #Gold #PreciousMetals #FederalReserve #Inflation #FOMC #OilPrices #GoldDemand #CentralBanks #WealthPreservation #MacroOutlook #Commodities #FinancialAdvisors #PortfolioDiversification #Geopolitics