WiseGold Weekly Pulse | June 5, 2026

Coverage Period: May 29, 2026 (00:00:00 EST) to Jun 5, 2026 (11:00:00 EST)

WiseGold Capital partners with advisors to assist them in managing assets for their clients. WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Nothing in this publication constitutes investment advice.

Executive Summary

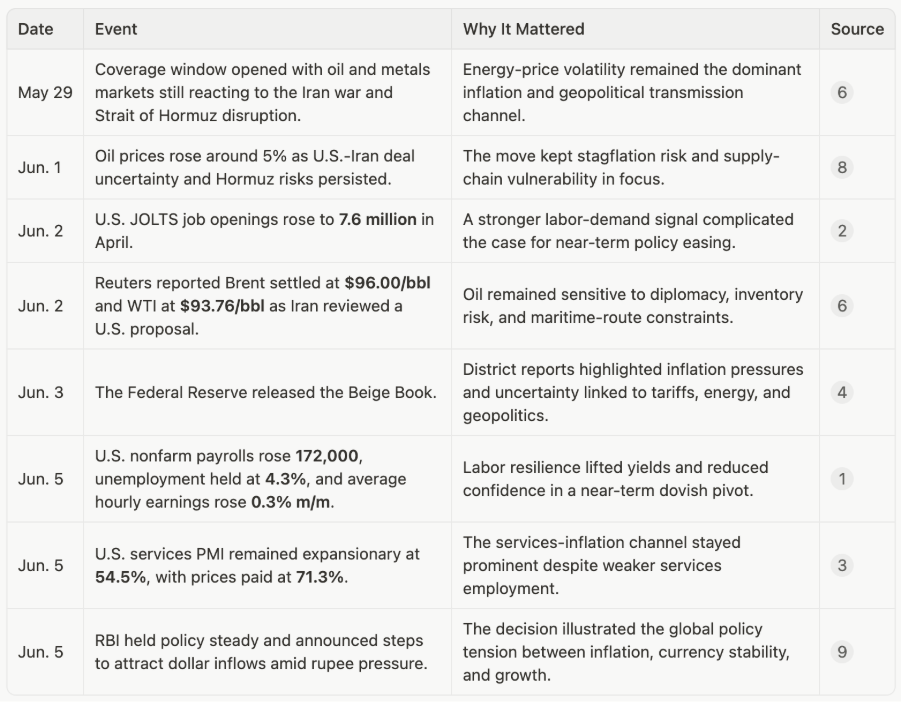

The week’s macro message was resilience under pressure. U.S. payrolls beat expectations, services activity improved, job openings rose, and the Federal Reserve’s Beige Book continued to describe inflation pressures tied to energy and geopolitical disruption. At the same time, oil volatility, a still-fragile Strait of Hormuz backdrop, and higher Treasury yields reinforced a more hawkish market interpretation of policy risk.1 2 3 4

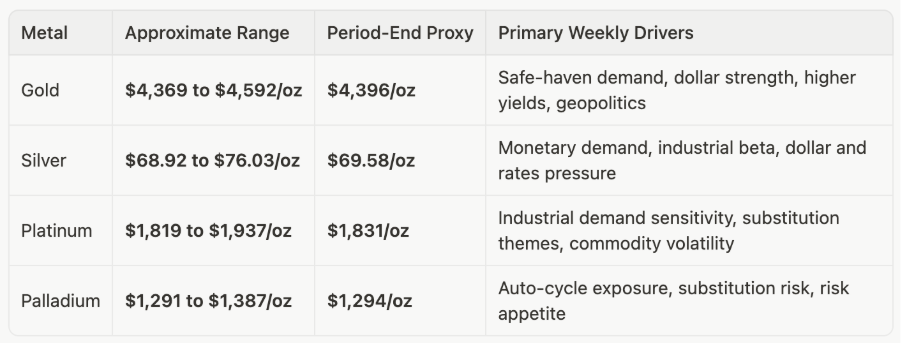

Precious metals traded as a risk-hedging complex but faced crosscurrents from a firmer dollar and rising real-rate expectations. Gold futures traded roughly $4,369 to $4,592/oz, silver roughly $68.92 to $76.03/oz, platinum roughly $1,819 to $1,937/oz, and palladium roughly $1,291 to $1,387/oz during the measurement window used for market ranges.5

Key takeaways:

- Policy risk re-priced higher. Strong U.S. labor data and sticky services prices reduced confidence that disinflation would proceed smoothly.1 3

- Energy remained the macro hinge. Brent traded roughly $91.46 to $99.00/bbl, while WTI traded roughly $86.35 to $97.00/bbl, with Hormuz-related disruption still central to risk premia.5 6

- The dollar firmed. The U.S. Dollar Index futures proxy traded roughly 98.75 to 99.86, supported by resilient U.S. data, higher oil prices, and geopolitical safe-haven demand.5 7

- Metals retained strategic relevance. The case for precious metals remains rooted in diversification, liquidity, financial resilience, and non-sovereign store-of-value attributes, not short-term trading direction.

Market & Macro Week-in-Review Timeline

Thematic Deep Dives

Monetary Policy: Central Banks Face the Energy-Inflation Constraint

Central-bank reaction functions moved further away from a clean easing narrative. The Fed’s June policy meeting was still ahead, but the week’s data pushed investors toward a more hawkish interpretation. Strong payrolls, firm earnings growth, resilient services demand, and elevated services prices all made the policy path more sensitive to incoming inflation data.1 3

Global central-bank commentary also suggested that the broad rate-cutting cycle had lost momentum. KPMG’s June central-bank scanner described a world in which energy shocks and geopolitical constraints were forcing policymakers to revisit inflation risks, with the ECB and Fed expected to remain cautious and the Bank of Japan still confronting normalization pressure.10

The Reserve Bank of India’s decision to hold rates steady showed the same dilemma in emerging-market form. Reuters reported that the RBI faced falling-currency pressure, oil-related external strain, and inflation concerns, while also announcing measures aimed at attracting dollar inflows and supporting the rupee.9

Growth, Inflation, Employment, and PMI: U.S. Resilience Remained the Baseline

The U.S. labor market delivered a stronger signal than expected. Nonfarm payrolls rose 172,000 in May, the unemployment rate held at 4.3%, labor-force participation was 61.8%, and average hourly earnings increased 0.3% month over month and 3.4% year over year. March and April payrolls were revised higher by a combined 93,000.1

Labor demand also looked firmer in the JOLTS data. April job openings increased by 731,000 to 7.6 million, while hires declined to 5.1 million, total separations declined to 5.0 million, quits were 3.0 million, and layoffs and discharges were 1.7 million.2

The services side of the economy remained expansionary. ISM Services PMI rose to 54.5%, with business activity at 57.7% and new orders at 57.3%. The weakness was employment at 47.9%, while the prices-paid index jumped to 71.3%, the highest reading since August 2022.3

Rates and Yield Curve: Strong Data Lifted the Front-End Sensitivity Narrative

Treasury yields rose into the end of the period as stronger payrolls shifted the near-term policy narrative. The 10-year Treasury yield proxy traded roughly 4.43% to 4.55%, ending near 4.54% in the market-range data set. A 5-year yield proxy traded roughly 4.12% to 4.29%, ending near 4.28%.5

The curve message was not simply about growth optimism. It reflected a combination of persistent inflation uncertainty, energy-price risk, and reduced confidence that the Fed would validate easier financial conditions quickly. Reuters’ June 5 market coverage, referenced in its news index, characterized the strong May jobs number as pushing yields and rate expectations higher.6

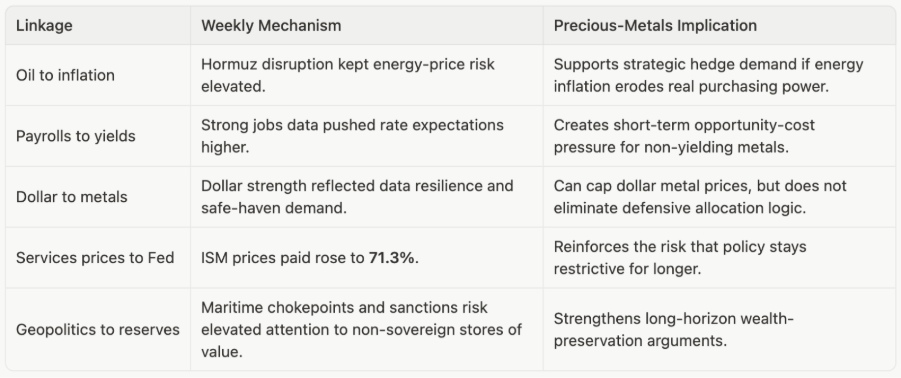

For precious metals, higher yields represent a near-term opportunity-cost headwind. Yet the same driver can also strengthen strategic demand when rising rates reflect fiscal, inflation, or geopolitical stress rather than clean real-growth improvement.

FX and Dollar Landscape: The Dollar Recovered Support from Data and Risk Demand

The dollar’s tone improved through the week. The U.S. Dollar Index futures proxy traded roughly 98.75 to 99.86, closing near the upper end of that range. Convera attributed the dollar’s firmness to higher oil prices, a flatter U.S. curve, solid U.S. data, and renewed Middle East tension.5 7

EUR/USD remained range-bound near 1.16 to 1.1650 in Convera’s commentary, while FXStreet noted that EUR/USD traded near 1.1613 on June 5 as geopolitical uncertainty and restrictive-policy expectations supported the dollar.7 11

For gold and silver, the FX channel was mixed. A stronger dollar can restrain dollar-denominated metals prices, but dollar strength tied to energy shock, geopolitical stress, or safe-haven demand does not automatically negate metals’ defensive role.

Energy and Broader Commodities: Oil Was the Macro Transmission Channel

Energy remained the central cross-asset risk factor. Reuters reported that Brent rose to $96.00/bbl and WTI to $93.76/bbl on June 2 as Iran reviewed a U.S. proposal and the Strait of Hormuz remained largely shut to maritime traffic. Reuters also reported that the strait typically affects about one-fifth of global oil and liquefied natural gas flows.6

CNBC framed the Hormuz standoff as a shift in the energy-security debate. The article argued that the protracted closure exposed fossil-fuel supply-chain fragility, while also elevating policy attention toward domestic power generation, batteries, renewables, and energy-system resilience.12

In market-range data, Brent traded roughly $91.46 to $99.00/bbl, WTI roughly $86.35 to $97.00/bbl, and U.S. natural gas futures roughly $3.10 to $3.40/MMBtu. The broader commodity backdrop therefore remained consistent with inflation uncertainty rather than clean disinflation.5

Precious Metals Focus

Gold traded roughly $4,369 to $4,592/oz during the period. The metal remained caught between safe-haven demand and headwinds from a stronger dollar and higher yields. FXStreet noted that gold was near $4,450/oz in early European trading on June 5, awaiting the U.S. employment report and remaining sensitive to U.S.-Iran developments.11

Silver traded roughly $68.92 to $76.03/oz. Silver continued to behave as both a monetary and industrial metal, which made it sensitive to the same dual forces shaping the week: safe-haven demand on one side and rate-sensitive growth expectations on the other.5

Platinum traded roughly $1,819 to $1,937/oz, while palladium traded roughly $1,291 to $1,387/oz. The platinum-group metals complex remained more exposed to cyclical, automotive, substitution, and supply-chain themes than gold. In a week dominated by rates, FX, and energy, PGM performance reflected broader commodity volatility more than a pure monetary-hedge narrative.5

Cross-Asset Interlinkages

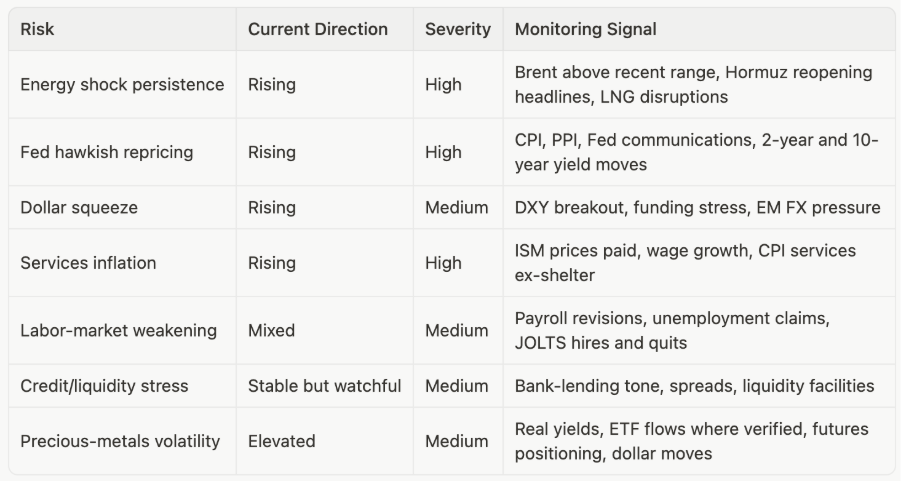

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

The next major catalyst set is inflation-heavy. The BLS calendar showed CPI and real earnings due June 10 and PPI due June 11. These releases will help determine whether stronger activity data can coexist with disinflation or whether markets must price a longer period of restrictive policy.13

The Fed’s June meeting will follow a week in which payrolls, JOLTS, and services prices argued against complacency. Any communication that validates higher-for-longer rates would likely strengthen the dollar and challenge metals tactically. Conversely, acknowledgement of growth downside or financial fragility could reintroduce support for defensive assets.

Energy diplomacy remains equally important. Any material reopening of the Strait of Hormuz could reduce oil-risk premia, while a renewed escalation would likely transmit through inflation expectations, FX, and safe-haven demand.

Portfolio Context & Implications

For diversified portfolios, the week reinforced the importance of distinguishing tactical price pressure from strategic function. Higher yields and a firmer dollar can weigh on precious metals over shorter horizons. However, the same week also demonstrated why many allocators continue to evaluate metals as part of a broader financial-resilience framework.

Gold’s strategic role is not dependent on a single weekly price move. It is tied to liquidity, global recognition, low credit risk, and historical use as a reserve and private wealth-preservation asset. Silver adds higher volatility and industrial sensitivity, while platinum and palladium add distinct cyclical and supply-chain exposures.

This report does not recommend trades, allocations, leverage, or timing. It frames the macro backdrop that advisors and professional investors may use as one input in broader due diligence.

Precious Metals Strategic Thesis

The strategic thesis for precious metals remains grounded in diversification, wealth protection, preservation, and financial resilience. A week defined by energy chokepoints, resilient labor data, central-bank caution, and currency pressure underscored the value of assets that are not direct liabilities of a bank, government, or corporate issuer.

Gold remains the core monetary metal in this framework. Silver provides a hybrid monetary-industrial exposure. Platinum and palladium can broaden the metals sleeve but carry more direct cyclical and automotive-linked sensitivities.

The long-term case is therefore not a forecast that metals must rise immediately. It is the observation that metals can serve as a portfolio ballast when inflation uncertainty, geopolitical disruption, currency volatility, or institutional-trust risks become more prominent.

Summary Capsule

The week ended with stronger U.S. labor data, firmer services activity, higher services prices, and a more hawkish rates tone. Oil and Hormuz risks remained central, while the dollar strengthened alongside resilient U.S. data and safe-haven demand. Precious metals faced short-term pressure from yields and FX but retained strategic relevance as diversification and resilience assets in an unsettled macro regime.

Methodology & Notes

This report uses information available through the cutoff of Friday, June 5, 2026, 11:00 AM EDT. The coverage period begins at Friday, May 29, 2026, 00:00:00 EDT and ends at the stated publication cutoff. Market ranges are based on publicly accessible daily futures and index-proxy data retrieved during report preparation and should be treated as approximate, not as official settlement data.5

All figures are reported with units where applicable. Macro data are sourced from primary releases where available, including BLS and ISM. News and market interpretation are sourced from Reuters, CNBC, Convera, FXStreet, KPMG, and Anadolu Agency. No unverifiable ETF-flow tonnage, central-bank purchase data, or positioning claims are included.

Disclosure

This material is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any security, commodity, currency, derivative, or precious-metals product. Precious metals and related assets involve risk, including price volatility and possible loss of principal. Readers should consult qualified financial, tax, legal, and other professional advisors before making any financial decision. WiseGold Capital partners with advisors to assist them in managing assets for their clients, but WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Past performance is not indicative of future results.

Source List

[1] BLS, Employment Situation, June 5, 2026

[2] BLS, Job Openings and Labor Turnover Survey, June 2, 2026

[3] ISM, Services PMI, May 2026

[4] Federal Reserve, Beige Book, June 3, 2026

[5] Yahoo Finance public chart endpoint, market-range data retrieved June 5, 2026

[6] Reuters, Oil prices rise to one-week high as Iran reviews U.S. proposal, June 2, 2026

[7] Convera, Buckle up for U.S. jobs report, June 5, 2026

[9] Reuters, Indian central bank keeps policy rate on hold, June 5, 2026

[10] KPMG, June 2026 Central Bank Scanner

[11] FXStreet, EUR/USD: All eyes on Nonfarm Payrolls, June 5, 2026

[12] CNBC, How the Strait of Hormuz standoff flipped the energy security debate, June 5, 2026

[13] BLS, June 2026 Economic Release Calendar

#WiseGold #Gold #Silver #PreciousMetals #MacroStrategy #MarketInsights #WealthPreservation #PortfolioDiversification #FinancialResilience #Inflation #MonetaryPolicy #Commodities #Geopolitics #FamilyOffice #FinancialAdvisors #AssetAllocation #WiseGoldCapital