When the Dollar Roars and Gold Stumbles: What This Week’s Market Storm Means for Wealth Preservation

WiseGold Weekly Pulse | June 26, 2026

Coverage Period: Jun 20, 2026 (00:00:00 EST) to Jun 26, 2026 (11:00:00 EST)

WiseGold Capital partners with advisors to assist them in managing assets for their clients. WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Nothing in this publication constitutes investment advice.

About WiseGold

The WiseGold Weekly Pulse is published by WiseGold, a consulting and logistics firm that partners with financial advisors, family offices, and money managers to facilitate access to physical precious metals as part of a broader wealth preservation and portfolio diversification framework. Additional resources, including institutional-grade market commentary, educational content on precious metals fundamentals, and information on WiseGold’s advisory support services, are available at https://wise.gold.

Executive Summary

The past week witnessed a significant recalibration in global financial markets, driven by shifting monetary policy expectations and easing geopolitical tensions. The Federal Reserve, under the new leadership of Chairman Kevin Warsh, delivered a hawkish pause, projecting a rate hike by year-end 2026 in response to persistent inflation [1]. This pivot propelled the U.S. Dollar Index to a one-year high and lifted Treasury yields, creating substantial headwinds for the precious metals complex [2]. Concurrently, a provisional ceasefire between the U.S. and Iran led to the reopening of the Strait of Hormuz, precipitating a sharp decline in crude oil prices to pre-war levels and reducing the geopolitical risk premium across asset classes [3]. Despite the near-term pressure on gold and silver, structural demand from central banks remains robust, with a record 45% planning to increase their gold reserves over the next twelve months [4].

Key Takeaways:

- Fed’s Hawkish Pivot: Chairman Warsh signals a potential rate hike in 2026, driving dollar strength [1].

- Geopolitical De-escalation: U.S.-Iran ceasefire reopens the Strait of Hormuz, easing oil prices [3].

- Precious Metals Pullback: Gold breaches $4,000/oz support amid rising yields and dollar momentum [5].

- Central Bank Accumulation: A record 45% of central banks plan to expand gold reserves [4].

- U.K. Political Transition: Prime Minister Keir Starmer resigns, paving the way for new leadership [6].

Market & Macro Week-in-Review Timeline

- Sat Jun 20: Iran’s Khatam Al-Anbiya Central Headquarters announces compliance with international law regarding the Strait of Hormuz [7].

- Mon Jun 22: U.K. Prime Minister Keir Starmer announces his resignation, with Andy Burnham emerging as the likely successor [6].

- Tue Jun 23: Nornickel projects a 300,000-ounce global palladium surplus for 2026, citing weaker automotive demand [8].

- Wed Jun 24: The U.S. and Iran agree to a roadmap for a final peace deal, leading to the reopening of the Strait of Hormuz [3].

- Wed Jun 24: Gold breaches the $4,000/oz threshold for the first time since November 2025, pressured by a stronger dollar [5].

- Thu Jun 25: U.S. Q1 GDP growth is revised upward to 2.1% annualized, reflecting economic resilience [9].

- Thu Jun 25: Initial jobless claims fall to 215,000, indicating a stable labor market [10].

- Fri Jun 26: University of Michigan Consumer Sentiment Index final reading for June shows improvement over May (10:00) [11].

- Fri Jun 26: U.S. PCE inflation data released, showing a 4.1% year-over-year increase in May (10:00) [12].

Thematic Deep Dives

Macro & Monetary Policy

The Federal Reserve maintained the federal funds rate at 3.50% to 3.75% but adopted a markedly hawkish stance under new Chairman Kevin Warsh. The updated Summary of Economic Projections indicates a median expectation of a rate hike by the end of 2026, a significant departure from previous easing biases [1]. Chairman Warsh also announced sweeping institutional reforms, including the elimination of forward guidance, signaling a return to a purely data-dependent approach [1]. Meanwhile, the ECB raised its key interest rates by 25 basis points to combat inflation driven by recent energy shocks [13].

Inflation & Growth Data

U.S. economic growth demonstrated resilience, with Q1 2026 GDP revised upward to 2.1% annualized [9]. However, inflation remains a persistent challenge. The Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation gauge, rose 4.1% year-over-year in May, while core PCE advanced 3.4% [12]. This sticky inflation data reinforces the Fed’s higher-for-longer narrative. Conversely, the S&P Global Flash U.S. Composite PMI rose to 52.2 in June, indicating continued expansion in business activity [14].

Rates & Yield Curve Dynamics

Treasury yields experienced volatility, initially rising on the Fed’s hawkish signals before stabilizing. The 10-year Treasury yield hovered around 4.40%, while the 2-year yield remained elevated, reflecting expectations of tighter monetary policy [15]. The yield curve inversion has rapidly shrunk to approximately 27 basis points, driven by a steepening trend that suggests markets are adjusting to the prospect of sustained higher short-term rates [16].

FX & Dollar Landscape

The U.S. Dollar Index (DXY) broke out of its recent range, hitting a one-year high above 100.50 [2]. This strength is underpinned by the Fed’s hawkish pivot and a widening interest rate differential favoring the U.S. over other major economies. The euro faced downward pressure following the ECB’s rate hike, which was accompanied by a cautious economic outlook [13]. The Japanese yen remained weak, trading above 160 against the dollar, despite the Bank of Japan’s minor rate increase [17].

Energy & Broader Commodities Context

Energy markets experienced a significant repricing following the provisional ceasefire between the U.S. and Iran. Brent crude oil fell to approximately $73 per barrel, its lowest level since before the conflict escalated in February, as the reopening of the Strait of Hormuz alleviated supply concerns [18]. Natural gas futures crept higher due to warmer weather forecasts boosting demand for electric power generation [19].

Precious Metals Focus

The precious metals complex faced intense pressure from the surging U.S. dollar and elevated Treasury yields.

- Gold: Traded roughly $3,990 to $4,190/oz, breaking below the $4,000 support level [5].

- Silver: Traded roughly $55.60 to $65.50/oz, suffering a steep percentage decline [5].

- Platinum: Traded roughly $1,555 to $1,661/oz, pressured by a stronger dollar [5].

- Palladium:Traded roughly $1,155 to $1,243/oz, weighed down by surplus projections [5].

Despite near-term price weakness, physical gold-backed ETFs saw $1.1 billion in inflows during the week [20]. Furthermore, a World Gold Council survey revealed that a record 45% of central banks plan to increase their gold reserves over the next year, highlighting strong structural demand [4].

Credit & Liquidity

Credit markets remained relatively stable, with high-yield corporate bond spreads holding steady around 2.71% [21]. The Fed’s commitment to maintaining ample reserves in the banking system, as reaffirmed during the June FOMC meeting, continues to support overall market liquidity [1].

Equity & Volatility Sentiment

U.S. equities experienced a pullback, particularly in the technology sector, as markets digested the implications of higher interest rates. The S&P 500 and Nasdaq Composite posted consecutive daily declines, though year-to-date gains remain robust [22]. The CBOE Volatility Index (VIX) edged higher to around 18.6, reflecting a modest increase in market anxiety [23].

Geopolitics & Strategic Risk

The geopolitical landscape saw a significant de-escalation with the U.S. and Iran agreeing to a roadmap for a peace deal, effectively reopening the Strait of Hormuz to international shipping [3]. In the U.K., Prime Minister Keir Starmer announced his resignation, introducing a period of political transition as the Labour Party seeks a new leader [6].

Structural & Long-Term Themes

The integration of artificial intelligence continues to drive capital expenditure and productivity expectations, particularly in the technology sector [1]. Additionally, the upcoming U.S. midterm elections in November 2026 are beginning to draw focus, with potential implications for fiscal policy and regulatory frameworks [24].

Cross-Asset Interlinkages

- The U.S.-Iran ceasefire directly precipitated a sharp decline in crude oil prices, which in turn reduced the inflation risk premium embedded in long-term bond yields [18].

- The Federal Reserve’s hawkish pivot catalyzed a breakout in the U.S. Dollar Index, creating a direct headwind for dollar-denominated commodities, notably gold and silver [2].

- Rising Treasury yields increased the opportunity cost of holding non-yielding assets, amplifying the selloff in the precious metals complex [5].

- The projected surplus in the palladium market by Nornickel compounded the macro-driven weakness, leading to underperformance relative to platinum [8].

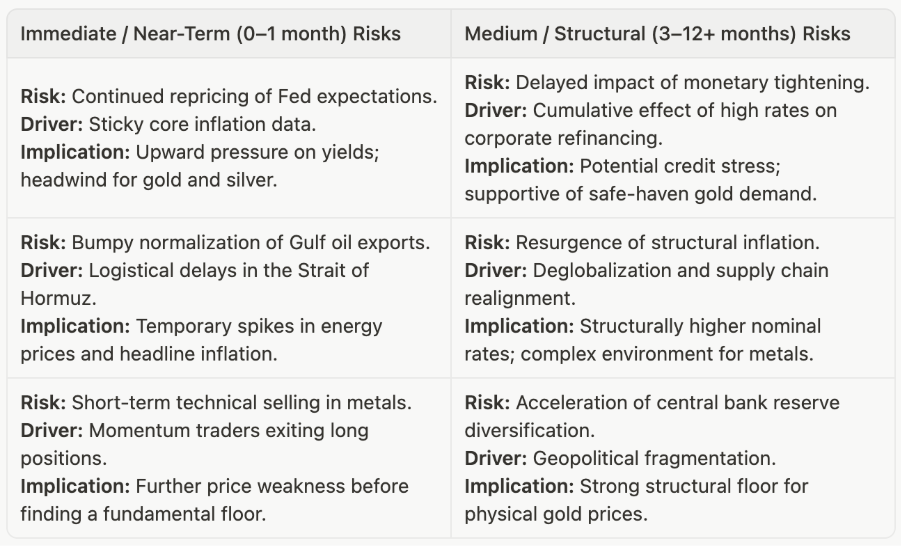

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

- U.S. Employment Data (Base Probability): Upcoming non-farm payrolls will be critical in confirming the labor market’s resilience and the Fed’s policy path.

- U.S.-Iran Final Agreement (Elevated Probability): Successful conclusion of the 60-day negotiation period would solidify the geopolitical de-escalation, maintaining downward pressure on oil.

- Central Bank Gold Purchases (Base Probability): Continued accumulation by emerging market central banks will provide underlying support for gold prices.

- Precious Metals Sensitivity Note: A hawkish surprise in upcoming inflation data equals a potential headwind to bullion.

Portfolio Context & Implications

The recent pullback in precious metals, driven by macroeconomic headwinds, contrasts with the robust structural demand from central banks. This divergence may offer a strategic entry point for long-term allocators seeking diversification. The evolving monetary policy landscape, characterized by higher-for-longer interest rates, underscores the importance of holding assets that can provide a hedge against systemic risks and currency debasement.

Precious Metals Strategic Thesis

Diversification Attribute

Precious metals maintain a low correlation to traditional financial assets, providing essential portfolio diversification, particularly during periods of equity market volatility or shifting monetary policy expectations.

Wealth Protection & Purchasing Power

Historically, gold and silver have served as reliable stores of value, protecting purchasing power against the erosive effects of inflation and fiat currency depreciation.

Drawdown Mitigation & Crisis Optionality

The inherent safe-haven characteristics of precious metals offer crucial downside protection during geopolitical crises or severe market dislocations, enhancing overall portfolio resilience.

Structural Demand Drivers

The fundamental outlook for precious metals is supported by sustained central bank accumulation, growing industrial applications (particularly for silver in green technologies), and constrained mine supply.

Allocation Framing

Academic research and historical performance suggest that a strategic allocation to precious metals can improve risk-adjusted returns by dampening portfolio volatility and providing a hedge against tail risks.

Summary Capsule

- Macro Pulse: The Fed adopts a hawkish stance under new leadership, projecting a rate hike in 2026.

- Metals Stance: Gold and silver face near-term pressure from a surging dollar and rising yields.

- Risk Tone: Geopolitical risks ease following a provisional U.S.-Iran ceasefire.

- Positioning Nuance: Central banks signal strong intent to increase gold reserves over the next year.

- Forward Watch: Markets will monitor upcoming U.S. labor data and the progress of U.S.-Iran negotiations.

- Structural Theme: Persistent inflation and shifting monetary frameworks dominate the long-term outlook.

Source List

[1] American Deposit Management — FOMC June Meeting Summary: Stable Rates, Sweeping Institutional Reforms — June 23, 2026 — https://americandeposits.com/insights/2026-june-fomc-meeting-stable-rates-reforms/ [2] Convera — US Dollar ignores falling oil prices, hits one-year high — June 24, 2026 — https://convera.com/blog/market-insights/fx-research/daily-market-updates/us-dollar-ignores-falling-oil-prices-hits-one-year-high/ [3] NPR — U.S. and Iran agree to ‘road map’ for final deal, mediators say — June 21, 2026 — https://www.npr.org/2026/06/21/g-s1-129222/us-iran-deal-lebanon-israel-strait-hormuz-jd-vance [4] World Gold Council — Central Bank Gold Reserves Survey 2026 — June 16, 2026 — https://www.gold.org/goldhub/research/central-bank-gold-reserves-survey-2026 [5] Texas Precious Metals — Precious Metals Market Update: 6/24/2026 — June 24, 2026 — https://texmetals.com/all-news/precious-metals-market-update-6-24-2026 [6] NPR — U.K. Prime Minister Keir Starmer announces resignation — June 22, 2026 — https://www.npr.org/2026/06/22/nx-s1-5866231/keir-starmer-resigns [7] Doha News via Instagram — Iran’s Khatam Al-Anbiya Central Headquarters — June 20, 2026 — https://www.instagram.com/reel/DZz22i1KeW7/ [8] Nornickel — Nornickel presents metals market review — June 23, 2026 — https://nornickel.com/news-and-media/press-releases-and-news/nornickel-presents-metals-market-review-230626/ [9] Reuters — US first-quarter GDP revised sharply higher — June 25, 2026 — https://www.reuters.com/business/us-first-quarter-gdp-revised-sharply-higher-consumer-spending-nearly-stalls-2026-06-25/ [10] Reuters — US weekly jobless claims drop more than expected — June 25, 2026 — https://www.reuters.com/business/us-weekly-jobless-claims-drop-more-than-expected-2026-06-25/ [11] Washington Post — Consumer spending resilient in the face of quickly rising prices — June 25, 2026 — https://www.washingtonpost.com/business/2026/06/25/consumer-spending-resilient-face-quickly-rising-prices/ [12] Reuters — May US PCE inflation tops 4%, leaves Fed hike on the table — June 25, 2026 — https://www.reuters.com/markets/us/us-pce-inflation-measure-tops-40-may-consumer-spending-strong-2026-06-25/ [13] European Central Bank — Our monetary policy statement at a glance — June 2026 — June 2026 — https://www.ecb.europa.eu/press/press_conference/visual-mps/2026/html/mopo_statement_explained_june.en.html [14] Wall Street Journal — U.S. Business Activity Continued to Expand in June — June 23, 2026 — https://www.wsj.com/economy/u-s-business-activity-continued-to-expand-in-june-b7982f07 [15] CNBC — 10-year Treasury yield falls below 4.5% as oil falls to pre-war levels — June 24, 2026 — https://www.cnbc.com/2026/06/24/treasury-yields-oil-falls-pre-war-levels.html [16] Kamakura Corporation — SAS Weekly Treasury Simulation, June 19, 2026 — June 22, 2026 — https://www.kamakuraco.com/sas-weekly-treasury-simulation-june-19-2026-25-probability-of-inverted-yields-by-march-2027/ [17] DailyForex — Weekly Forex Forecast — USD/JPY, USD/CAD, NASDAQ 100 Index, Gold, WTI Crude Oil — June 21, 2026 — https://www.dailyforex.com/forex-technical-analysis/2026/06/weekly-forex-forecast-21st-to-26th-june-2026/246671 [18] Reuters — Brent settles at lowest since before start of Iran war — June 24, 2026 — https://www.reuters.com/business/energy/oil-prices-extend-decline-expectations-smoother-crude-flows-via-hormuz-2026-06-24/ [19] Natural Gas Intel — Natural Gas Futures Creeping Higher as Forecasts Add Demand — June 26, 2026 — https://naturalgasintel.com/news/natural-gas-futures-creeping-higher-as-forecasts-add-demand/ [20] Cointelegraph via Facebook — LATEST: Gold-backed ETFs recorded $1.1 billion in inflows last week — June 23, 2026 — https://www.facebook.com/cointelegraph/posts/%EF%B8%8F-latest-gold-backed-etfs-recorded-11-billion-in-inflows-last-week-the-largest-w/1327064496267042/ [21] StreetStats — Corporate Bonds — Investment Grade & High Yield Bond Interest Rates — June 23, 2026 — https://streetstats.finance/rates/corporates [22] Investopedia — Markets News, June 25, 2026: Nasdaq Slides as Tech Giants… — June 25, 2026 — https://www.investopedia.com/stock-market-today-dow-jones-s-and-p-500-06252026-12006401 [23] FRED — CBOE Volatility Index: VIX — June 26, 2026 — https://fred.stlouisfed.org/series/VIXCLS [24] The Economist — US House of Representatives 2026 forecast — June 26, 2026 — https://www.economist.com/interactive/2026/us-midterms/prediction-model/house

Methodology & Notes

Data for this report was compiled from a diverse array of publicly available, credible financial news sources, central bank communications, and economic data releases. Price ranges for precious metals are approximated based on intraday highs and lows reported during the coverage window. The coverage period explicitly includes data releases up to 11:00 AM EST on Friday, June 26, 2026, capturing key economic indicators such as the University of Michigan Consumer Sentiment Index and the PCE inflation report.

Disclosure

This report is for informational purposes only and does not constiute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instrument. The views expressed are based on publicly available information believed to be reliable, but accuracy or completeness cannot be guaranteed. Past performance is not indicative of future results. Readers should conduct their own analysis and consult qualified professionals before making any financial decisions.

#WiseGold #Gold #PreciousMetals #MacroEconomics #WealthPreservation #FinancialResilience #FederalReserve #Inflation #CentralBanks #FinancialAdvisors #FamilyOffice #WealthManagement #MarketIntelligence #WiseGoldCapital