WiseGold Weekly Pulse | June 19, 2026

Coverage Period: Jun 13, 2026 (00:00:00 EST) to Jun 19, 2026 (11:00:00 EST)

WiseGold Capital partners with advisors to assist them in managing assets for their clients. WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Nothing in this publication constitutes investment advice.

About WiseGold

The WiseGold Weekly Pulse is published by WiseGold, a consulting and logistics firm that partners with financial advisors, family offices, and money managers to facilitate access to physical precious metals as part of a broader wealth preservation and portfolio diversification framework. Additional resources, including institutional-grade market commentary, educational content on precious metals fundamentals, and information on WiseGold’s advisory support services, are available at https://wise.gold.

Executive Summary

The past week was defined by a profound collision of hawkish monetary policy recalibration and a historic geopolitical de-escalation, triggering a rapid repricing across global asset classes. The Federal Reserve, under the new leadership of Chairman Kevin Warsh, held interest rates steady but delivered a hawkish surprise by removing projected 2026 rate cuts from its “dot plot,” signaling a commitment to price stability over near-term easing [1] [2]. Concurrently, the official signing of a U.S.-Iran ceasefire agreement and the prospective reopening of the Strait of Hormuz precipitated a sharp decline in energy prices, collapsing the geopolitical risk premium that had previously buoyed crude oil and precious metals [3] [4]. This dual shock, combining higher-for-longer U.S. interest rates with fading Middle East conflict premiums, drove a significant selloff in the precious metals complex, with gold, silver, platinum, and palladium all registering notable declines as the U.S. dollar strengthened and Treasury yields surged [5] [6]. Despite these near-term headwinds, robust U.S. retail sales and stabilizing consumer sentiment underscore underlying economic resilience [7] [8].

Key Takeaways

- Fed Pivots Hawkish: Chairman Warsh signals “higher for longer,” removing 2026 rate cut projections entirely [2].

- Geopolitical De-escalation: U.S.-Iran peace deal signing triggers a sharp drop in global crude oil prices [3] [4].

- Metals Face Headwinds: Surging yields and a stronger dollar drive broad selloffs across the precious metals complex [5].

- Consumer Resilience: Strong May retail sales challenge expectations of an imminent economic slowdown [7].

- ECB Tightens First: The European Central Bank raised rates by 25 bps on June 12, the first G7 central bank to hike in the current cycle, citing energy-driven inflation [21].

Market & Macro Week-in-Review Timeline

- Thu Jun 11 (prior period, ongoing influence): The European Central Bank raises its deposit rate by 25 bps to 2.25%, becoming the first G7 central bank to hike in the current cycle, citing energy-driven inflation at 10.9% and a revised 2026 eurozone inflation forecast of 3.0% [21].

- Fri Jun 12: Market anticipation builds ahead of the FOMC meeting; early reports circulate regarding potential progress in U.S.-Iran peace negotiations, initiating downward pressure on energy markets [3] [9].

- Mon Jun 15: The Bank of Japan raises its short-term policy rate to 1.00%, marking a historic tightening move and lifting borrowing costs to levels unseen since 1995 [10].

- Tue Jun 16: U.S. May retail sales data is released, showing a robust 0.9% increase, surpassing expectations and highlighting consumer resilience despite elevated inflation [7].

- Wed Jun 17: The Federal Reserve holds rates at 3.50% to 3.75%. The updated dot plot reveals a hawkish shift, removing the previously projected 2026 rate cut. Precious metals sell off sharply in response [1] [2] [5].

- Thu Jun 18: The Bank of England maintains its Bank Rate at 3.75% [11]. Initial U.S. jobless claims fall slightly to 226,000, confirming continued labor market tightness [12].

- Fri Jun 19: (10:00) U.S. financial markets are closed for the Juneteenth holiday [13]. The formal signing of the U.S.-Iran ceasefire agreement takes place in Geneva, cementing the geopolitical de-escalation [3].

Thematic Deep Dives

Macro & Monetary Policy

The monetary policy landscape experienced a seismic shift this week, led by the Federal Reserve’s decisive hawkish pivot.

- The FOMC held the federal funds rate at 3.50% to 3.75%, but the revised Summary of Economic Projections eliminated the median forecast for a 2026 rate cut [1] [2].

- The Bank of Japan delivered a historic rate hike to 1.00%, signaling a definitive end to its ultra-loose monetary policy era [10].

- The Bank of England opted to hold rates steady at 3.75%, balancing inflation concerns against economic growth risks [11].

Under Chairman Kevin Warsh, the Federal Reserve has clearly prioritized inflation containment over preemptive easing. The removal of the 2026 rate cut projection from the dot plot caught markets off guard, prompting a rapid upward repricing of short-term interest rate expectations. This synchronized global tightening, punctuated by the BOJ’s historic move, underscores a durable “higher for longer” regime that continues to challenge non-yielding assets.

Inflation & Growth Data

Economic indicators released this week painted a picture of persistent inflation coupled with surprising consumer strength.

- U.S. May retail sales increased by a robust 0.9%, significantly beating the consensus estimate of 0.6% [7].

- U.S. CPI inflation for the year ended May 2026 registered at 4.2%, confirming that price pressures remain elevated above central bank targets [14].

- Initial jobless claims ticked down to 226,000, indicating that the labor market remains structurally tight [12].

The combination of strong retail sales and a resilient labor market complicates the disinflationary narrative. While the U.S.-Iran peace deal offers the prospect of lower energy-driven inflation in the coming months, the current data confirms that underlying demand remains robust. This resilience provides the Federal Reserve with the necessary economic cover to maintain its restrictive policy stance without immediate fear of inducing a recession.

Rates & Yield Curve Dynamics

The hawkish FOMC outcome triggered a sharp reaction across the U.S. Treasury curve.

- The 2-year Treasury yield surged by more than 16 basis points to roughly 4.21% immediately following the Fed announcement [5].

- The 10-year Treasury yield advanced to approximately 4.46%, reflecting the market’s recalibration of long-term policy expectations [5].

- The yield curve remains inverted, though the short end experienced the most pronounced upward pressure.

The rapid repricing of the Treasury curve reflects the market’s capitulation to the Fed’s revised guidance. The surge in the 2-year yield, which is highly sensitive to near-term policy expectations, illustrates the evaporation of rate-cut optimism. These elevated nominal yields, assuming inflation expectations remain anchored, translate to higher real yields, creating a formidable structural headwind for precious metals.

FX & Dollar Landscape

The U.S. dollar asserted its dominance this week, propelled by the divergence in global monetary policy expectations.

- The U.S. Dollar Index (DXY) strengthened, climbing toward the 100.80 level as yield differentials favored the greenback [15].

- The Japanese yen faced renewed pressure, nearing 40-year lows against the dollar despite the BOJ’s rate hike, as the U.S.-Japan yield gap remains exceptionally wide [16].

- The euro traded lower, dipping below the 1.15 level against the dollar amid the broader greenback rally [16].

The dollar’s strength is a direct corollary of the Federal Reserve’s hawkish dot plot revision. As U.S. rates are projected to remain elevated relative to other major economies, capital flows continue to favor dollar-denominated assets. This currency dynamic acts as a dual depressant for precious metals, making them more expensive for international buyers while simultaneously reflecting the attractiveness of competing U.S. fixed-income instruments.

Energy & Broader Commodities Context

Energy markets experienced a dramatic repricing driven entirely by geopolitical developments.

- Brent crude oil prices tumbled significantly, breaking below the $80 per barrel threshold in response to the U.S.-Iran peace agreement [4].

- The prospective reopening of the Strait of Hormuz promises to alleviate the severe supply constraints that had previously driven prices above $100 per barrel [4] [9].

- Broader commodity indices reflected the energy-led drag, though some industrial metals showed resilience.

The formalization of the U.S.-Iran ceasefire represents a massive deflation of the geopolitical risk premium in energy markets. While the physical return of stranded barrels will take time, the market has rapidly priced in the normalization of Gulf exports. This sharp decline in energy costs should eventually filter through to headline inflation metrics, potentially altering the central bank calculus in the medium term, even as current policy remains restrictive.

Precious Metals Focus

The precious metals complex faced a perfect storm of rising yields, a stronger dollar, and fading geopolitical anxiety.

- Gold: Traded in a volatile range, ultimately falling from above $4,300 to close the week near $4,165/oz [5] [17].

- Silver: Experienced sharp percentage declines, dropping from near $70 to approximately $64.26/oz [5] [17].

- Platinum: Retreated significantly, settling near $1,709/oz as industrial demand concerns compounded macro headwinds [5].

- Palladium: Declined to roughly $1,304/oz, reflecting its high sensitivity to automotive sector dynamics [5].

- Positioning & Flows: Indian gold demand showed complex dynamics; a record 15% import duty temporarily compressed official imports, but ETF flows reversed from outflows to strong net inflows in early June, suggesting resilient underlying demand [17].

The synchronized selloff across the precious metals complex highlights the asset class’s vulnerability to real interest rate shocks. The evaporation of the geopolitical risk premium, which had heavily supported gold and silver during the height of the Middle East tensions, left the metals exposed to the hawkish Fed repricing. However, the rapid normalization of physical premiums in key markets like India suggests that strategic, price-sensitive buyers are utilizing the pullback to accumulate physical ounces.

Credit & Liquidity

Credit markets absorbed the rate shock with relative composure, indicating an absence of systemic stress.

- Investment-grade corporate bond yields rose in tandem with Treasuries, hovering around 5.13% [15].

- High-yield spreads remained relatively contained, reflecting confidence in corporate balance sheets despite higher borrowing costs [15].

- Overall financial conditions remain tight but orderly, with no immediate signs of liquidity dysfunction.

The resilience of corporate credit spreads suggests that equity and bond investors do not currently foresee a severe economic contraction. The market’s interpretation appears to be that the economy is strong enough to withstand the Fed’s “higher for longer” stance. This contained credit risk environment reduces the immediate safe-haven appeal of precious metals, forcing them to trade primarily on their inverse relationship with real yields.

Equity & Volatility Sentiment

Equity markets displayed a complex reaction function, balancing higher rates against economic resilience.

- The S&P 500 and Nasdaq indices demonstrated resilience, with technology and semiconductor stocks leading periodic rallies [8].

- The CBOE Volatility Index (VIX) remained subdued, trading near the 16.40 level, indicating a lack of panic among equity investors [15].

- The highly anticipated SpaceX IPO experienced early volatility, with shares dropping roughly 6% after an initial surge, highlighting selective market exuberance [18].

The subdued level of the VIX, despite the significant monetary policy surprise, points to a market that is pricing in a “soft landing” scenario. Equity investors are currently rewarding growth and earnings resilience over the threat of elevated discount rates. For precious metals, this buoyant risk sentiment detracts from their role as a portfolio hedge against severe market dislocations.

Geopolitics & Strategic Risk

The geopolitical landscape shifted dramatically from acute crisis to formal de-escalation.

- The United States and Iran officially signed a 14-point memorandum of understanding in Geneva, establishing a ceasefire and framework for peace [3].

- The agreement includes provisions for the reopening of the Strait of Hormuz, removing a critical choke point for global energy supplies [3] [9].

- While the immediate conflict has paused, the long-term strategic realignment in the Middle East remains complex and unresolved.

The U.S.-Iran peace deal is the defining geopolitical event of the quarter. It has systematically removed the extreme tail-risk scenarios that had driven safe-haven flows into gold and energy markets. However, the underlying structural rivalries in the region persist. Investors must recognize that while the acute crisis premium has been excised from asset prices, the baseline level of global geopolitical friction remains higher than in the previous decade.

Structural & Long-Term Themes

Long-horizon themes continue to operate beneath the surface of near-term volatility.

- De-dollarization: The narrative of shifting global reserve preferences persists, though the U.S. dollar’s current cyclical strength masks any immediate structural erosion [19].

- AI Investment: Capital expenditure in artificial intelligence continues to be a dominant driver of equity market performance and corporate strategy [20].

- Energy Transition: The volatility in fossil fuel prices underscores the complex, non-linear path of the global energy transition.

While the dollar currently benefits from the Fed’s hawkish stance, the long-term trend of central banks diversifying their reserves away from a unipolar dollar system remains a core structural support for physical gold. The immediate price action is dominated by rates, but the strategic rationale for holding non-sovereign reserve assets continues to build quietly in the background.

Cross-Asset Interlinkages

- Fed Hawkishness -> Yield Surge -> Dollar Strength -> Metals Weakness: The removal of the 2026 rate cut projection drove Treasury yields higher, which in turn strengthened the U.S. dollar, creating a dual headwind that forced the entire precious metals complex lower.

- Geopolitical Peace -> Oil Collapse -> Inflation Expectations Cool: The U.S.-Iran ceasefire agreement triggered a sharp selloff in crude oil, which should eventually translate to lower headline inflation, potentially altering the long-term trajectory of monetary policy.

- Resilient Consumer -> Tight Labor Market -> “Higher for Longer” Validated: Strong retail sales and low jobless claims provided the fundamental economic justification for the Federal Reserve to maintain its restrictive stance without triggering a credit event.

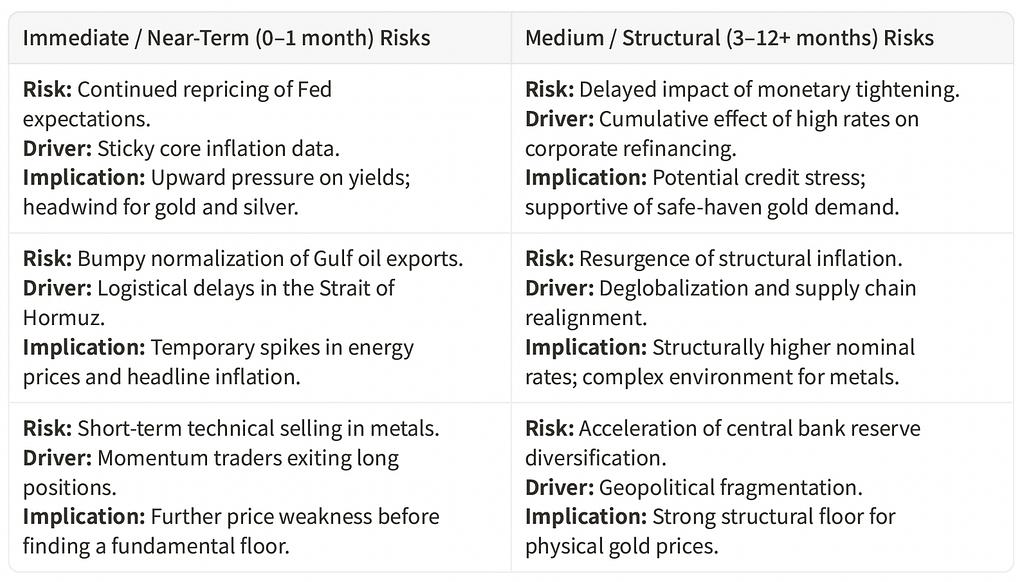

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

- Incoming U.S. Inflation Data (Base Probability): Upcoming PCE and CPI prints will be scrutinized to validate the Fed’s hawkish shift. A hotter-than-expected reading would solidify the “no cut” narrative, extending pressure on metals.

- Implementation of U.S.-Iran Peace Terms (Elevated Probability): The physical reopening of the Strait of Hormuz and the resumption of normal tanker traffic will dictate the final settling point for crude oil prices, indirectly impacting inflation expectations.

- Emergence of Credit Market Stress (Low-Probability Tail): Should the “higher for longer” regime suddenly trigger unexpected defaults in the high-yield or commercial real estate sectors, safe-haven flows could rapidly reverse the recent weakness in precious metals.

Portfolio Context & Implications

The events of the past week vividly illustrate the dual nature of precious metals within a diversified portfolio. When real interest rates rise and geopolitical fears recede, metals face intense downward pressure, as seen in the recent price action. However, this volatility underscores their role as an uncorrelated asset class. The current pullback, driven by a rapid recalibration of monetary policy expectations, may present strategic entry points for investors focused on long-term wealth preservation. The fundamental rationale for holding physical metals (protection against currency debasement and structural systemic risk) remains intact, even as cyclical forces dictate near-term pricing. WiseGold Capital continues to partner with advisors to navigate these complex market dynamics, providing the logistical framework necessary for strategic physical allocations.

Precious Metals Strategic Thesis

Diversification Attribute

Precious metals serve as a vital counterweight to traditional financial assets. Their recent underperformance in the face of rising yields highlights their lack of correlation with buoyant equity markets, fulfilling their role as a distinct asset class that behaves differently during various phases of the economic cycle.

Wealth Protection & Purchasing Power

While gold yields no interest, its historical function is to preserve purchasing power over extended horizons. The current environment of elevated nominal rates challenges this attribute in the short term, but the persistent underlying reality of fiat currency depreciation supports the long-term thesis for physical bullion.

Drawdown Mitigation & Crisis Optionality

The rapid deflation of the geopolitical risk premium this week demonstrates how quickly crises can resolve. However, the presence of gold in a portfolio provides perpetual optionality against unforeseen systemic shocks, functioning as an insurance policy that cannot be defaulted upon.

Structural Demand Drivers

Beyond Western investment flows, the structural demand for gold remains robust. The ongoing trend of central bank reserve diversification, particularly among emerging market economies, provides a durable foundation for physical demand that operates independently of U.S. monetary policy fluctuations.

Allocation Framing

Strategic allocations to precious metals are typically framed not as tactical trading vehicles, but as foundational portfolio anchors. Historical and academic analyses suggest that a measured allocation to physical metals can enhance risk-adjusted returns over full market cycles by reducing overall portfolio volatility and providing liquidity during periods of severe market stress.

Summary Capsule

- Macro Pulse: The Federal Reserve executed a hawkish pivot, removing 2026 rate cut projections and signaling a durable “higher for longer” regime.

- Metals Stance: The complex suffered a broad, synchronized selloff driven by surging Treasury yields, a stronger U.S. dollar, and the evaporation of geopolitical risk premiums.

- Risk Tone: Equity and credit markets remain resilient, pricing in a soft landing and absorbing the rate shock without displaying systemic stress.

- Positioning Nuance: Physical demand in key markets like India shows resilience, with buyers utilizing price dips and normalizing premiums to accumulate ounces.

- Forward Watch: Attention shifts to incoming inflation data to validate the Fed’s stance, and the logistical realities of reopening the Strait of Hormuz.

- Structural Theme: Despite near-term cyclical headwinds from high real rates, the long-term thesis of central bank reserve diversification away from the dollar remains a core support for gold.

Source List

[1] Federal Reserve — Federal Reserve issues FOMC statement — June 17, 2026 — https://www.federalreserve.gov/newsevents/pressreleases/monetary20260617a.htm [2] Yahoo Finance — Fed ‘dot plot’: Almost half of FOMC members project at least one interest rate hike this year — June 17, 2026 — https://finance.yahoo.com/economy/policy/article/fed-dot-plot-almost-half-of-fomc-members-project-at-least-one-interest-rate-hike-this-year-183645064.html [3] Democracy Now — Headlines for June 18, 2026 — June 18, 2026 — https://www.democracynow.org/2026/6/18/headlines [4] Reuters — Mapping the Market: Tumbling global oil price could fall further — June 18, 2026 — https://www.reuters.com/markets/global-markets-technicals-2026-06-18/ [5] Texas Precious Metals — Precious Metals Market Update: 6/18/2026 — June 18, 2026 — https://texmetals.com/all-news/precious-metals-market-update-6-18-2026 [6] Texas Precious Metals — Precious Metals Market Update: 6/17/2026 — June 17, 2026 — https://texmetals.com/all-news/precious-metals-market-update-6-17-2026 [7] Reuters — Strong US retail sales showcase economy’s resilience despite Iran war — June 17, 2026 — https://www.reuters.com/business/retail-consumer/us-retail-sales-beat-expectations-may-2026-06-17/ [8] Investopedia — Stock Market Today: Stock Futures Point To Rebound After Fed Sell-Off — June 18, 2026 — https://www.investopedia.com/stock-market-today-dow-jones-s-and-p-500-06182026-12001491 [9] Saxo Bank — Oil retreats as peace hopes rise but depleted inventories may limit the downside — June 16, 2026 — https://www.home.saxo/content/articles/commodities/oil-retreats-as-peace-hopes-rise-but-depleted-inventories-may-limit-the-downside-16062026 [10] Reuters — Bank of Japan hikes rates to 1%, highest since 1995 — June 15, 2026 — https://www.reuters.com/world/asia-pacific/bank-japan-set-raise-rates-31-year-high-vow-further-increases-2026-06-15/ [11] Bank of England — Bank Rate maintained at 3.75% — June 2026 Monetary Policy Summary — June 18, 2026 — https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2026/june-2026 [12] Reuters — US weekly jobless claims stay elevated amid seasonal volatility — June 18, 2026 — https://www.reuters.com/business/us-weekly-jobless-claims-fall-amid-low-layoffs-2026-06-18/ [13] LiveMint — Juneteenth 2026: What’s open and closed? — June 19, 2026 — https://www.livemint.com/news/us-news/juneteenth-2026-whats-open-and-closed-find-out-if-banks-usps-stock-markets-and-retail-stores-are-operating-11781874411876.html [14] Bureau of Labor Statistics — Consumer prices up 4.2 percent over the year ended May 2026 — June 17, 2026 — https://www.bls.gov/opub/ted/2026/consumer-prices-up-4-2-percent-over-the-year-ended-may-2026.htm [15] StreetStats — Corporate & High Yield Bond Yields and Spreads — June 18, 2026 — https://streetstats.finance/rates/corporates [16] Reuters — Yen teeters on cusp of 40-year low, pound bounces — June 19, 2026 — https://www.reuters.com/world/asia-pacific/yen-nears-weakest-40-years-boj-hike-fails-stem-rout-2026-06-19/ [17] USAGOLD — Gold Retreats to $4,165 on Geneva Signing; India’s Record 15% Import Duty Dents Physical Demand — June 19, 2026 — https://www.usagold.com/daily-precious-metals-market-report-june-19-2026/ [18] Forbes — SpaceX Shares Drop 6% In First Decline Since Historic IPO — June 17, 2026 — https://www.forbes.com/sites/tylerroush/2026/06/17/spacex-shares-drop-6-in-first-decline-since-historic-ipo/ [19] Brookings Institution — Is the US dollar’s reserve currency status eroding? — June 17, 2026 — https://www.brookings.edu/articles/is-the-us-dollars-reserve-currency-status-eroding/ [20] T. Rowe Price — 2026 Midyear Market Outlook: Five shifts reshaping markets — June 18, 2026 — https://www.troweprice.com/en/us/insights/global-market-outlook [21] World Socialist Web Site — European Central Bank lifts interest rate amid rising inflation — June 12, 2026 — https://www.wsws.org/en/articles/2026/06/13/iqau-j13.html

Methodology & Notes

This report synthesizes macroeconomic data, central bank policy announcements, geopolitical developments, and market pricing across multiple asset classes to provide a comprehensive overview of the factors influencing precious metals. Price ranges and daily changes are approximated based on available market data at the time of compilation. The coverage period extends through 11:00 AM EST on Friday, June 19, 2026, incorporating relevant morning data releases where available. Note that U.S. financial markets were closed on Friday, June 19, in observance of Juneteenth. CFTC Commitment of Traders (COT) data for the period was not published within the coverage window; positioning data is therefore noted as unavailable for this edition. ETF flow data is referenced where verifiable third-party sources were available.

Disclosure

This report is for informational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instrument. The views expressed are based on publicly available information believed to be reliable, but accuracy or completeness cannot be guaranteed. Past performance is not indicative of future results. Readers should conduct their own analysis and consult qualified professionals before making any financial decisions.

#WiseGold #PreciousMetals #Gold #MacroEconomics #FederalReserve #MonetaryPolicy #WealthManagement #FinancialAdvisors #FamilyOffice #PortfolioStrategy #MarketOutlook #WiseGoldCapital