WiseGold Weekly Pulse | July 3, 2026

Coverage Period: Jun 27, 2026 (00:00:00 EST) to Jul 3, 2026 (11:00:00 EST)

WiseGold Capital partners with advisors to assist them in managing assets for their clients. WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Nothing in this publication constitutes investment advice.

About WiseGold

The WiseGold Weekly Pulse is published by WiseGold, a consulting and logistics firm that partners with financial advisors, family offices, and money managers to facilitate access to physical precious metals as part of a broader wealth preservation and portfolio diversification framework. Additional resources, including institutional-grade market commentary, educational content on precious metals fundamentals, and information on WiseGold’s advisory support services, are available at https://wise.gold.

Executive Summary

The past week was characterized by cooling labor markets, persistent central bank caution, and easing geopolitical tensions, all of which drove cross-asset repricing. The U.S. labor market showed notable cooling, with June nonfarm payrolls rising by just 57,000 and the unemployment rate dipping to 4.2% primarily due to a decline in labor force participation [1]. Federal Reserve Chairman Kevin Warsh, speaking at the ECB Forum in Sintra, declined to provide forward guidance on rates but emphasized that inflation remains “too high,” maintaining a firm commitment to the 2% target [2]. Meanwhile, oil prices retreated following a U.S.-Iran ceasefire memorandum of understanding that eased fears of supply disruptions in the Strait of Hormuz [3]. Precious metals experienced a resurgence, with gold breaking above $4,100/oz and posting its first weekly gain in a month as investors dialed back expectations for further Fed rate hikes [4]. The broader macro environment suggests a transition toward slower growth and a potential peak in the U.S. dollar, reinforcing the strategic case for precious metals as a core portfolio diversifier.

Key Takeaways:

- Cooling Labor Market: U.S. June payrolls disappointed at 57,000, signaling a slowdown in job creation [1].

- Fed Remains Cautious: Fed Chair Warsh reiterated commitment to 2% inflation, resisting calls for premature rate cuts [2].

- Geopolitical Easing: A U.S.-Iran ceasefire MoU reduced oil supply risks, leading to a drop in crude prices [3].

- Gold Rebounds: Gold prices rose above $4,100/oz as markets scaled back near-term rate hike expectations [4].

- Dollar Weakness: The DXY slipped below the 100 mark, signaling a potential shift in the global funding environment [5].

Market & Macro Week-in-Review Timeline

- Fri Jun 26: Core PCE inflation for May was reported at 3.4%, with headline PCE at 4.1%, indicating persistent price pressures (note: this data was released June 25–26 but continued to shape market sentiment throughout the coverage week) [6].

- Mon Jun 29: The U.S. Supreme Court ruled 5–4 that Fed Governor Lisa Cook can remain in her position, affirming central bank independence against presidential firing attempts [7].

- Tue Jun 30: The JOLTS report showed U.S. job openings held steady at 7.6 million in May, reflecting a stable but cooling labor demand [8].

- Wed Jul 1: Fed Chair Kevin Warsh, at the ECB Forum in Sintra, stated that prices remain “too high” and declined to signal the July rate decision [2]. ADP reported private sector employment increased by 98,000 jobs in June, below expectations [9]. The ISM Manufacturing PMI registered 53.3%, down from May, showing easing factory activity [10].

- Thu Jul 2: The U.S. Labor Department reported June nonfarm payrolls increased by only 57,000, with the unemployment rate at 4.2% [1]. The U.S. declined to renew the USMCA trade pact, opting for an annual review process [11].

- Fri Jul 3: U.S. stock and bond markets observed the Independence Day holiday, closing trading for the long weekend [12].

Thematic Deep Dives

Macro & Monetary Policy

Central banks remain focused on inflation, balancing tight policy against signs of economic cooling. At the ECB Forum in Sintra, Fed Chair Kevin Warsh firmly rejected forward guidance and reiterated that the Fed will not tolerate inflation above its 2% target, despite political pressures [2].

- Warsh emphasized a return to “first principles” and reliance on real-time data rather than conventional surveys [2].

- The Bank of England held rates at 3.75%, with Governor Andrew Bailey noting that rate cuts are not yet on the table [13].

- The ECB and other major central banks are maintaining restrictive stances as core inflation proves sticky [2].

Inflation & Growth Data

U.S. economic data revealed a clear moderation in growth momentum. The June jobs report was a significant downside surprise, adding only 57,000 jobs, while prior months were revised downward [1].

- The unemployment rate fell to 4.2%, but this was driven by a shrinking labor force participation rate, which dropped to 61.5% [1].

- May Core PCE inflation remained elevated at 3.4%, keeping pressure on the Fed [6].

- Manufacturing activity eased, with the ISM PMI dropping to 53.3% in June, reflecting slower new orders and production [10].

Rates & Yield Curve Dynamics

Treasury yields experienced volatility, ultimately moving lower following the weak employment data. The prospect of a near-term Fed rate hike diminished significantly.

- The 10-year Treasury yield hovered around 4.48%, while the 2-year yield dropped to near 4.13% following the jobs report [14].

- Markets have largely priced out a July rate hike and reduced the probability of a September hike to around 50–60% [1].

- The yield curve remains inverted, but the front end rallied as traders adjusted their policy expectations [14].

FX & Dollar Landscape

The U.S. dollar faced significant downward pressure, with the DXY index breaking below the psychological 100 level. This shift reflects changing interest rate differentials and a cooling U.S. economy.

- The DXY traded near 100.8, extending a broad selloff as markets reassessed the “higher-for-longer” rate narrative [5].

- A weaker dollar provides a supportive environment for emerging market assets and dollar-denominated commodities [5].

- The euro and yen saw relative strength, although the Bank of Japan’s policy normalization remains gradual [15].

Energy & Broader Commodities Context

Energy markets were dominated by geopolitical developments, specifically the easing of tensions in the Middle East.

- Brent crude fell to around $71.57/bbl, and WTI dropped to $68.58/bbl, marking significant monthly declines [3].

- A 14-point memorandum of understanding between the U.S. and Iran paused fighting and eased concerns over oil flows through the Strait of Hormuz [3].

- Natural gas prices trended lower, stabilizing near $3.215/MMBtu amid robust supply [16].

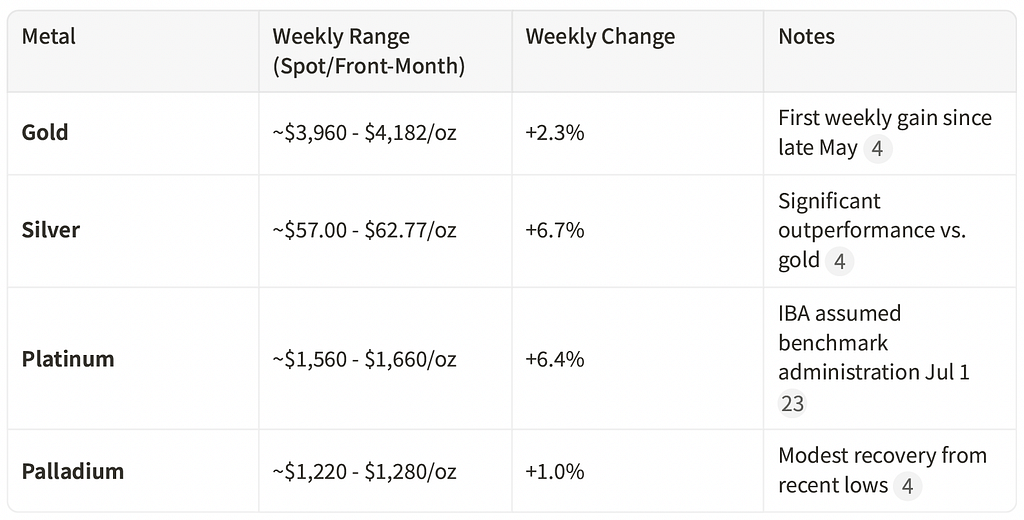

Precious Metals Focus

Precious metals rallied strongly as the U.S. dollar weakened and rate hike expectations moderated. The sector demonstrated resilience after a challenging second quarter, with all four metals posting gains on the week.

- Positioning data from the COT report (as of June 23, 2026) showed large speculators holding net long positions of approximately 181,339 contracts in gold futures, reflecting continued bullish sentiment despite recent price weakness [17].

- Positioning data for silver showed large speculators net long at approximately 23,751 contracts [17].

- ETF tonnage flows for the week ending July 3, 2026 were not fully published within the coverage window. [Verification Needed]

- Central bank gold demand: No new verifiable evidence of central bank purchases was published within the coverage window. The World Gold Council’s annual survey (published June 2026) noted that more global central banks are positioned to increase gold reserves over the next year [21].

Credit & Liquidity

Credit markets remained relatively stable, though the weak jobs report prompted a reassessment of corporate fundamentals.

- Investment-grade corporate bond yields stood at 5.19%, with a spread of 0.76% over Treasuries [18].

- High-yield spreads remain contained, but a sustained economic slowdown could lead to spread widening.

- Liquidity conditions are adequate, though the Fed’s ongoing quantitative tightening continues to drain reserves from the system.

Equity & Volatility Sentiment

U.S. equities experienced a mixed week, balancing weaker economic data against the prospect of lower interest rates.

- The S&P 500 closed near 7,483, showing slight declines as technology stocks faced profit-taking [19].

- The VIX index remained relatively subdued around 16.45, indicating that equity markets have not yet priced in significant recessionary risks [20].

- Trading volumes were lighter ahead of the July 4th holiday weekend [12].

Geopolitics & Strategic Risk

Geopolitical risks moderated slightly with the U.S.-Iran ceasefire, but structural uncertainties remain high.

- The U.S.-Iran MoU provided temporary relief to energy markets, but the situation remains fragile [3].

- The U.S. decision not to renew the USMCA trade pact introduces long-term uncertainty into North American trade relations [11].

- The upcoming U.S. midterm elections are increasingly viewed as a source of policy volatility [21].

Structural & Long-Term Themes

Long-term structural themes continue to shape the macro landscape, particularly the impact of artificial intelligence and fiscal sustainability.

- AI-driven capital expenditure is supporting economic growth, but its broad productivity benefits are still materializing [22].

- U.S. fiscal deficits and debt sustainability remain a core concern for long-term bond investors, supporting the structural case for real assets [22].

- De-dollarization trends, while gradual, continue to support central bank gold accumulation as a diversification strategy [15].

Cross-Asset Interlinkages

- Weaker Jobs -> Lower Yields -> Higher Gold: The disappointing June payrolls report led to a drop in short-term Treasury yields, reducing the opportunity cost of holding non-yielding gold and driving prices above $4,100/oz.

- Geopolitical Easing -> Lower Oil -> Reduced Inflation Fears: The U.S.-Iran ceasefire MoU caused crude oil prices to drop, which may help moderate headline inflation in the coming months, giving central banks more flexibility.

- Dollar Weakness -> Broad Commodity Support: The DXY slipping below 100 provided a tailwind for commodities across the board, particularly precious metals, making them cheaper for non-U.S. buyers.

- Sticky Core Inflation -> Central Bank Caution: Despite weaker growth data, elevated Core PCE inflation (3.4%) keeps the Fed and ECB cautious, preventing a rapid pivot to rate cuts and keeping real yields relatively high.

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

- U.S. CPI Data Release (Mid-July): [Base Probability] Expected to show gradual moderation. A hotter-than-expected print would revive rate hike fears, presenting a near-term headwind to bullion.

- FOMC Meeting (July 28–29): [Base Probability] Expected to hold rates steady. Markets will scrutinize the statement for any shifts in the balance of risks between inflation and employment.

- Breakdown of U.S.-Iran Ceasefire: [Elevated Probability] Given historical tensions, a resumption of hostilities would quickly spike oil prices and drive safe-haven flows into gold and the dollar.

- Significant Downward Revision to Q2 GDP: [Low-Probability Tail] A sharp contraction in growth would force the Fed to pivot dovish, leading to a rapid depreciation of the dollar and a strong rally in precious metals.

Portfolio Context & Implications

The current macroeconomic environment, characterized by slowing growth, sticky inflation, and elevated geopolitical risks, underscores the importance of robust portfolio construction. The recent breakdown in the U.S. dollar and the cooling labor market suggest that the peak in restrictive monetary policy may have passed. In this context, assets that provide non-correlated returns and protection against currency debasement become increasingly valuable. The resilience of precious metals during the recent period of high real yields highlights their structural underlying demand. As traditional equity-bond correlations face challenges in a potentially stagflationary environment, real assets and alternative diversifiers may play a crucial role in mitigating portfolio volatility and preserving purchasing power over the long term.

Precious Metals Strategic Thesis

Diversification Attribute

Gold’s low correlation to traditional risk assets makes it a vital diversifier. During periods of equity market stress or shifting monetary policy expectations, gold often provides a stabilizing force, reducing overall portfolio volatility.

Wealth Protection & Purchasing Power

As fiat currencies face long-term pressures from expansive fiscal policies and rising debt levels, precious metals serve as a proven store of value. Gold’s historical ability to maintain purchasing power makes it a critical hedge against inflation and currency debasement.

Drawdown Mitigation & Crisis Optionality

In times of acute geopolitical crisis or financial systemic stress, gold exhibits strong safe-haven characteristics. The recent price action during the Middle East tensions demonstrates gold’s utility in mitigating severe portfolio drawdowns.

Structural Demand Drivers

Beyond investment flows, gold benefits from robust structural demand. Central banks continue to accumulate gold reserves to diversify away from the U.S. dollar, while physical demand from Asian markets (particularly China and India) provides a strong fundamental floor for prices.

Allocation Framing

Academic research and historical performance analysis suggest that a strategic allocation to precious metals can enhance the risk-adjusted returns of a diversified portfolio. While the optimal allocation varies by investor profile, the inclusion of gold and silver provides a foundational layer of financial resilience.

Summary Capsule

- Macro Pulse: U.S. labor market cools significantly (57k jobs added in June), signaling a potential economic slowdown.

- Metals Stance: Gold breaks above $4,100/oz, posting its first weekly gain in a month as rate hike expectations recede.

- Risk Tone: Equity markets remain near highs but show signs of fatigue; VIX remains subdued despite underlying economic shifts.

- Positioning Nuance: COT data indicates large speculators are adding to net long positions in gold, reflecting renewed bullish momentum.

- Forward Watch: Focus shifts to upcoming U.S. CPI data and the late-July FOMC meeting for clarity on the Fed’s policy trajectory.

- Structural Theme: Persistent U.S. fiscal deficits and global de-dollarization trends provide long-term structural support for precious metals.

Source List

[1] Reuters — US job growth slows in June; unemployment rate falls to 4.2% amid decline in labor force — July 2, 2026 — https://www.reuters.com/world/us/us-job-growth-misses-expectations-june-unemployment-rate-falls-42-2026-07-02/ [2] CNBC — Fed Chief Kevin Warsh declines to hint at July rate decision, but says inflation ‘too high’ — July 1, 2026 — https://www.cnbc.com/2026/07/01/kevin-warsh-ecb-forum-live-updates.html [3] CNBC — Oil prices fall after Trump says U.S.-Iran talks in Qatar are going well — July 1, 2026 — https://www.cnbc.com/2026/07/01/oil-prices-brent-wti-crude-trump-iran.html [4] CNBC — Gold prices set for first weekly rise in a month as investors scale back Fed rate hike bets — July 3, 2026 — https://www.cnbc.com/2026/07/03/gold-silver-price-inflation-fed-rate-hike.html [5] E8 Markets — Dollar Breakdown: What DXY Below 100 Means for FX, Stocks, and Commodities — July 2, 2026 — https://blog.e8markets.com/article/dollar-breakdown-what-dxy-below-100-means-for-fx-stocks-and-commodities [6] Forum Nadlan — Core Inflation Hits 3.4% in May 2026 — June 26, 2026 — https://www.forumnadlanusa.com/2026/06/core-pce-inflation-may-2026/ [7] Reuters — Fed’s Warsh vows to ‘disappoint’ anyone who thinks he will tolerate inflation above 2% — July 1, 2026 — https://www.reuters.com/world/europe/warsh-hits-international-stage-with-peers-sharing-an-inflation-problem-2026-07-01/ [8] Bureau of Labor Statistics — Job Openings and Labor Turnover Summary — 2026 M05 Results — June 30, 2026 — https://www.bls.gov/news.release/jolts.nr0.htm [9] ADP — ADP National Employment Report: Private Sector Employment Increased by 98,000 Jobs in June — July 1, 2026 — https://mediacenter.adp.com/2026-07-01-ADP-National-Employment-Report-Private-Sector-Employment-Increased-by-98,000-Jobs-in-June-Annual-Pay-was-Up-4-4 [10] PR Newswire — Manufacturing PMI® at 53.3%; June 2026 ISM® Manufacturing PMI® Report — July 1, 2026 — https://www.prnewswire.com/news-releases/manufacturing-pmi-at-53-3-june-2026-ism-manufacturing-pmi-report-302814991.html [11] TIME — U.S. Declines to Renew Trade Pact With Mexico And Canada — July 2, 2026 — https://time.com/article/2026/07/02/us-declines-renewal-trade-pact-mexico-canada-impact/ [12] MarketWatch — When Are Markets Closed for the July 4th Holiday? — July 2, 2026 — https://www.wsj.com/livecoverage/june-jobs-report-stock-market-07-02-2026/card/when-are-markets-closed-for-the-july-4th-holiday--3PNB1UAZIOT7jR4TK3E8 [13] Reuters — Rate cuts are not back on the table for Britain, Bank of England’s Bailey says — July 1, 2026 — https://www.reuters.com/world/uk/rate-cuts-are-not-back-table-britain-bank-englands-bailey-says-2026-07-01/ [14] CNBC — 2-year Treasury yield eases as light jobs report reduces Fed hike expectations — July 2, 2026 — https://www.cnbc.com/2026/07/02/us-treasury-yields-rise-as-investors-await-june-jobs-report.html [15] Morningstar — Will the US Dollar Rally Continue? — July 3, 2026 — https://global.morningstar.com/en-nd/markets/will-us-dollar-rally-continue [16] Sprague Energy — Natural Gas Contract Trends Analyzed for July — July 2, 2026 — https://www.spragueenergy.com/august-nymex-natural-gas-futures-contract-closed-at-3-220-on-wednesday-july-1st/ [17] GoldSeek — COT Gold, Silver & USDX Report — June 26, 2026 — June 26, 2026 — https://goldseek.com/article/cot-gold-silver-usdx-report-june-26-2026 [18] StreetStats — Corporate Bonds — Investment Grade & High Yield Bond Interest Rates — June 30, 2026 — https://streetstats.finance/rates/corporates [19] Yahoo Finance — Stock Market News for July 2, 2026 — July 2, 2026 — https://finance.yahoo.com/markets/stocks/articles/stock-market-news-july-2-132600808.html [20] FRED — CBOE Volatility Index: VIX — July 3, 2026 — https://fred.stlouisfed.org/series/VIXCLS [21] World Gold Council — Gold Mid-Year Outlook 2026: Point break — July 1, 2026 — https://www.gold.org/goldhub/research/gold-mid-year-outlook-2026 [22] iCapital — iCapital Market Pulse: The AI Economy’s Biggest Surprises — June 26, 2026 — https://icapital.com/insights/investment-market-strategy/icapital-market-pulse-the-ai-economys-biggest-surprises/ [23] LBMA — IBA to Administer LBMA Platinum and Palladium Price Benchmarks from 1 July 2026 — July 1, 2026 — https://www.lbma.org.uk/articles/iba-to-administer-lbma-platinum-and-palladium-price-benchmarks-from-1-july-2026

Pending Verification

- The exact volume of central bank gold purchases in June 2026, as comprehensive monthly data was not fully published within the coverage window.

- The specific ETF tonnage flows for GLD and other major gold ETFs for the exact week ending July 3, 2026.

- The most recent COT report data as of July 3, 2026, as the CFTC typically publishes the report on Fridays; the June 26, 2026 report (positions as of June 23) was the most recent available within the coverage window.

Methodology & Notes

- Data Compilation: Data was gathered from credible financial news sources, central bank publications, and market data providers covering the period from June 27, 2026 (00:00:00 EST) to July 3, 2026 (11:00:00 EST).

- Price Ranges: Precious metals prices are approximated based on spot market data available during the coverage window.

- Timestamp Conventions: All times referenced are Eastern Standard Time (EST) unless otherwise noted. Friday 10:00 AM EST data releases, such as the ISM Manufacturing PMI and JOLTS report (from earlier in the week), are incorporated.

Disclosure

This report is for informational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instrument. The views expressed are based on publicly available information believed to be reliable, but accuracy or completeness cannot be guaranteed. Past performance is not indicative of future results. Readers should conduct their own analysis and consult qualified professionals before making any financial decisions.

#WiseGold #PreciousMetals #Gold #Silver #WiseGold #MacroOutlook #WealthProtection #PortfolioDiversification #FinancialResilience #GoldMarket #WeeklyPulse #CentralBanks #Inflation #FederalReserve #MarketIntelligence #RealAssets #WiseGoldCapital