WiseGold Weekly Pulse | July 17, 2026

Coverage Period: Jul 11, 2026 (00:00:00 EST) to Jul 17, 2026 (11:00:00 EST)

WiseGold Capital partners with advisors to assist them in managing assets for their clients. WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Nothing in this publication constitutes investment advice.

About WiseGold

The WiseGold Weekly Pulse is published by WiseGold, a consulting and logistics firm that partners with financial advisors, family offices, and money managers to facilitate access to physical precious metals as part of a broader wealth preservation and portfolio diversification framework. Additional resources, including institutional-grade market commentary, educational content on precious metals fundamentals, and information on WiseGold’s advisory support services, are available at https://wise.gold.

Executive Summary

This week’s financial landscape was dominated by a sharp divergence between cooling domestic inflation data and an escalating geopolitical oil shock. The U.S. Consumer Price Index (CPI) for June came in softer than expected at 3.5% year-over-year, initially fueling expectations for Federal Reserve rate cuts [1]. However, a sudden intensification of the U.S.-Iran conflict, marked by military strikes and a renewed naval blockade of the Strait of Hormuz, sent crude oil prices surging over 9% to a multi-week high [2]. This supply-side shock immediately complicated the monetary policy outlook, as Fed Chair Kevin Warsh reiterated a “no tolerance” stance for persistently elevated inflation during his semiannual congressional testimony [3]. Consequently, markets rapidly repriced the probability of a July rate hike, lifting Treasury yields and the U.S. dollar, which in turn pressured the precious metals complex [4]. Despite the short-term headwinds from higher opportunity costs, the stagflationary undercurrents, cooling growth metrics paired with rising energy costs, reinforce the strategic thesis for gold as a critical portfolio diversifier and wealth preservation asset.

Key Takeaways

- Inflation cools, but energy risks loom: June CPI fell to 3.5% YoY, but surging oil threatens to reverse progress [1] [2].

- Fed pivots hawkish on oil shock: Rate cut hopes dashed as markets price in higher odds of a July hike [3] [4].

- Geopolitics drive market volatility: U.S.-Iran strikes disrupt Strait of Hormuz, spiking energy and safe-haven demand [2].

- Metals pressured by yields and dollar: Gold and silver pull back amid rising opportunity costs, though physical demand persists [4].

Market & Macro Week-in-Review Timeline

- Fri Jul 10: U.S. weekly jobless claims (week ended July 11) fall to 208,000, defying expectations, signaling continued labor market stability [22]. Prior-week equity market gains carry over into the session.

- Mon Jul 13: The U.S. and Iran exchange military strikes over the weekend; Iran targets vessels in the Strait of Hormuz, sending WTI crude up over 9% [2]. Precious metals sell off sharply on hawkish Fed commentary regarding inflation risks [4].

- Tue Jul 14: U.S. June CPI report shows headline inflation cooling to 3.5% YoY, driven by a temporary drop in energy prices that has since reversed [1]. Fed Chair Kevin Warsh testifies before the Senate, emphasizing the central bank’s commitment to the 2% target [3].

- Wed Jul 15: The Bank of Canada holds its policy rate at 2.25%, citing weaker-than-expected economic growth [6]. U.S. Producer Price Index (PPI) unexpectedly falls 0.3% in June, though the data precedes the recent oil spike [7].

- Thu Jul 16: U.S. retail sales rise a marginal 0.2% in June, reflecting cautious consumer spending [8]. The European Central Bank (ECB) signals it will hold rates steady next week but points to a potential September hike due to the energy price resurgence [9].

- Fri Jul 17 (10:00 AM): Preliminary University of Michigan Consumer Sentiment Index for July jumps to 54.4, beating expectations, though concerns remain over the renewed Middle East conflict [10]. U.S. housing starts rebound 19% in June, driven by multifamily construction, while single-family starts slip [11].

Thematic Deep Dives

Macro & Monetary Policy

Global central banks face a renewed dilemma as supply-side shocks threaten to derail disinflationary progress. In the U.S., Fed Chair Kevin Warsh’s congressional testimony underscored a firm commitment to price stability, noting that recent soft inflation data does not mean “mission accomplished” [3]. The Bank of Canada held its policy rate at 2.25%, balancing sluggish growth against persistent price pressures [6]. Meanwhile, the ECB is expected to maintain its deposit rate at 2.25% next week, though the recent surge in energy prices has increased the likelihood of a September hike [9]. The Bank of Korea also signaled an impending rate hike to combat inflation exacerbated by higher oil costs and a weaker won [12].

Inflation & Growth Data

June data presented a misleadingly benign picture of inflation, largely due to a temporary lull in energy prices. U.S. headline CPI rose 3.5% year-over-year, below expectations, while core CPI held at 2.6% [1]. The PPI also registered a surprising 0.3% monthly decline [7]. However, these figures predate the recent spike in crude oil. On the growth front, U.S. retail sales grew a tepid 0.2% in June, suggesting consumer caution [8], while housing starts showed a mixed picture with a rebound in multifamily units masking a slight decline in single-family construction [11].

Rates & Yield Curve Dynamics

The yield curve experienced a “bear steepening” as the geopolitical oil shock and hawkish Fed rhetoric prompted a repricing of interest rate expectations. The 10-year U.S. Treasury yield climbed to approximately 4.57%, while the 2-year yield hovered around 4.15%, maintaining a positive spread of roughly 42 basis points [13]. The market’s swift pivot from pricing in rate cuts to anticipating potential hikes reflects the heightened sensitivity to inflation risks and the realization that the Fed may be forced to keep rates “higher for longer.”

FX & Dollar Landscape

The U.S. dollar demonstrated resilience, supported by safe-haven flows and the prospect of tighter monetary policy. The DXY index traded near the 100.70 level, recovering from earlier weakness as the Middle East escalation prompted a flight to quality [14]. The stronger dollar acted as a headwind for commodities and emerging market currencies, complicating the inflation outlook for nations reliant on imported energy.

Energy & Broader Commodities Context

Energy markets were the epicenter of volatility this week. The collapse of an interim U.S.-Iran agreement and subsequent military strikes disrupted shipping in the critical Strait of Hormuz [2]. Brent crude futures surged past $84 per barrel, while WTI topped $80, reflecting a significant geopolitical risk premium [15]. This supply shock threatens to pass through to broader commodity prices and consumer inflation, presenting a major challenge for policymakers globally.

Precious Metals Focus

Precious metals faced significant headwinds from the rising U.S. dollar and higher Treasury yields during the coverage period. Gold traded in a range of roughly $4,012–$4,074/oz (spot), pulling back from recent highs as the paper market discounted the opportunity cost of holding non-yielding assets [4] [16]. Silver exhibited similar volatility, trading between approximately $56.70–$58.55/oz [4] [17]. Platinum traded near $1,593–$1,616/oz and palladium in the range of approximately $1,241–$1,277/oz [4] [17]. Despite the price weakness, physical demand remains robust, as investors recognize the stagflationary potential of the current macro environment. Positioning data indicates some unwinding of long positions in gold ETFs, with holdings falling to a nine-and-a-half-month low, reflecting the shift in rate expectations [4]. COT data for the week ended July 10 showed managed money net long positions in gold at approximately +116,161 contracts, suggesting positioning remains constructive but vulnerable to further liquidation if the hawkish repricing accelerates [23]. Central bank demand: No new verifiable central bank purchase data was published within the coverage window.

Credit & Liquidity

Credit conditions remain relatively stable, though the rapid repricing of interest rates poses risks for highly leveraged sectors. Corporate bond yields remain attractive, but the potential for further Fed tightening could lead to wider spreads and tighter liquidity in the coming months [18]. The banking sector reported strong Q2 earnings, driven by trading and investment banking revenues, suggesting resilience in the financial system despite the uncertain macro backdrop [19].

Equity & Volatility Sentiment

Equity markets exhibited a mixed performance, caught between solid corporate earnings and rising interest rate anxieties. The S&P 500 experienced marginal declines as investors rotated out of technology stocks, while the VIX volatility index remained subdued but prone to sudden spikes on geopolitical headlines [20]. The overarching theme of AI investment continues to support mega-cap tech valuations, though concerns about the sustainability of this trend are growing [21].

Geopolitics & Strategic Risk

The Middle East conflict re-emerged as the primary driver of global risk. The exchange of military strikes between the U.S. and Iran, coupled with disruptions in the Strait of Hormuz, has elevated the threat of a broader regional war [2]. This escalation not only impacts energy markets but also introduces significant uncertainty into global supply chains and trade routes, reinforcing the need for safe-haven assets.

Structural & Long-Term Themes

The massive capital expenditure cycle driven by artificial intelligence remains a dominant structural theme. Companies are investing heavily in AI infrastructure, data centers, and related technologies, which is expected to boost long-term productivity [21]. However, this buildout is also contributing to supply-demand imbalances in certain sectors, such as semiconductors and power generation, adding a unique layer of inflationary pressure to the economy [5].

Cross-Asset Interlinkages

- Geopolitics & Energy: The U.S.-Iran conflict directly caused a spike in crude oil prices, reintroducing a significant risk premium into the energy market.

- Energy & Rates: The surge in oil prices quickly translated into higher inflation expectations, prompting markets to reprice the probability of Fed rate hikes and driving Treasury yields higher.

- Rates & Precious Metals: Higher Treasury yields and a stronger U.S. dollar increased the opportunity cost of holding gold and silver, leading to a pullback in precious metals prices despite the underlying stagflationary risks.

- Equities & Tech: The structural theme of AI investment continues to support equity markets, particularly the technology sector, providing a counterbalance to the headwinds of higher interest rates and geopolitical uncertainty.

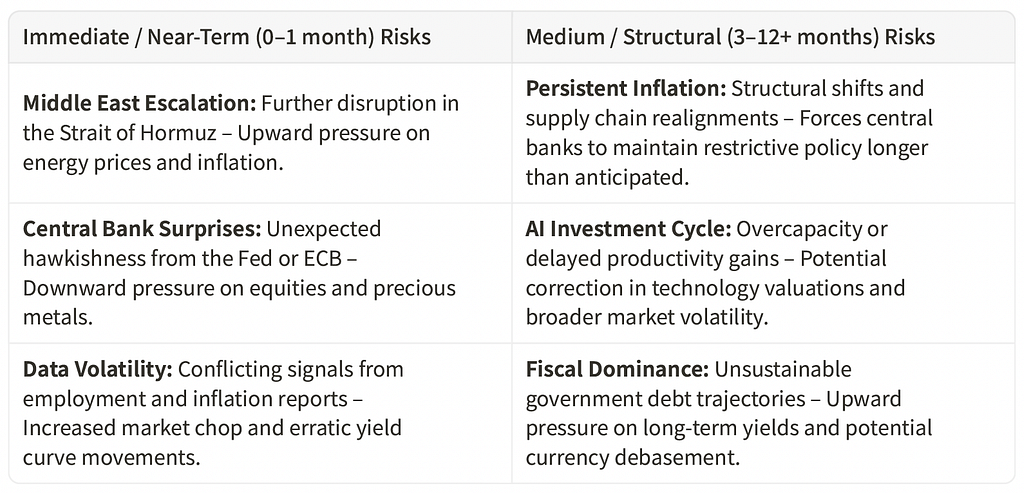

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

- ECB Policy Meeting (July 23): Base Probability. The ECB is expected to hold rates steady, but any hawkish guidance regarding a September hike could boost the euro and weigh on the dollar.

- FOMC Policy Meeting (July 28–29): Elevated Probability. Markets will closely scrutinize the Fed’s statement and Chair Warsh’s press conference for clues on the rate path. A hawkish surprise = potential headwind to bullion.

- Middle East Developments: Elevated Probability. Further military strikes or prolonged disruptions in the Strait of Hormuz could trigger another spike in oil prices, reinforcing stagflationary fears and supporting physical demand for precious metals.

Portfolio Context & Implications

The current macroeconomic environment, characterized by a collision of cooling domestic data and escalating geopolitical shocks, highlights the importance of robust portfolio construction. The rapid repricing of interest rate expectations and the resurgence of energy-driven inflation underscore the limitations of traditional 60/40 allocations. In this context, the strategic rationale for maintaining a diversified allocation to hard assets remains compelling. While paper market volatility may create short-term price fluctuations, the underlying fundamentals suggest that assets uncorrelated with monetary policy and geopolitical risk will play a crucial role in preserving purchasing power and mitigating drawdown risk.

Precious Metals Strategic Thesis

Diversification Attribute

Precious metals continue to demonstrate their value as non-correlated assets. During periods of acute geopolitical stress and shifting monetary policy expectations, gold and silver offer a counterbalance to the volatility inherent in equities and fixed income.

Wealth Protection & Purchasing Power

The resurgence of energy prices highlights the persistent threat of inflation. Gold’s historical role as a store of value makes it a vital tool for protecting purchasing power against the erosive effects of fiat currency debasement and supply-side price shocks.

Drawdown Mitigation & Crisis Optionality

The sudden escalation in the Middle East serves as a stark reminder of the unpredictable nature of global risks. Precious metals provide essential crisis optionality, acting as a financial anchor during periods of severe market dislocation or geopolitical instability.

Structural Demand Drivers

Beyond safe-haven appeal, precious metals benefit from structural demand drivers. Silver, platinum, and palladium are critical components in the green energy transition and advanced manufacturing, providing a fundamental floor to prices even amid macroeconomic headwinds.

Allocation Framing

From a historical and academic perspective, a strategic allocation to precious metals is viewed not as a speculative trade, but as a foundational element of a resilient portfolio. This allocation is designed to enhance risk-adjusted returns and provide long-term stability across various economic cycles.

Summary Capsule

- Macro Pulse: Cooling domestic inflation data collides with a severe geopolitical oil shock, complicating the central bank policy outlook.

- Metals Stance: Precious metals face short-term pressure from a stronger dollar and higher yields, but the physical market remains supported by stagflationary risks.

- Risk Tone: Elevated geopolitical uncertainty and the potential for “higher for longer” interest rates are driving market volatility.

- Positioning Nuance: Paper market selling in ETFs contrasts with robust physical demand as investors seek tangible wealth protection.

- Forward Watch: All eyes are on the upcoming ECB and FOMC meetings, as well as developments in the Strait of Hormuz, for directional cues.

- Structural Theme: The AI investment cycle continues to drive capital expenditure, while the energy transition underpins long-term industrial demand for silver and PGMs.

Source List

[1] Reuters — US consumer inflation moderates; upside risks remain amid renewed Middle East conflict — July 14, 2026 — https://www.reuters.com/business/us-consumer-inflation-slows-more-than-expected-june-2026-07-14/ [2] Reuters — US, Iran each attack infrastructure in risky escalation — July 17, 2026 — https://www.reuters.com/world/middle-east/iran-launches-fresh-attacks-after-sixth-day-us-strikes-2026-07-17/ [3] Wall Street Journal — Warsh Tells Congress the Fed Has ‘No Tolerance’ for High Inflation — July 14, 2026 — https://www.wsj.com/economy/central-banking/warsh-tells-congress-the-fed-has-no-tolerance-for-high-inflation-50c5dfa8 [4] Texas Precious Metals — Precious Metals Market Update: 7/13/2026 — July 13, 2026 — https://texmetals.com/all-news/precious-metals-market-update-7-13-2026 [5] Federal Reserve — Speech by Governor Cook on the economic outlook — July 15, 2026 — https://www.federalreserve.gov/newsevents/speech/cook20260715a.htm [6] Bank of Canada — Bank of Canada maintains the policy rate at 2¼% — July 15, 2026 — https://www.bankofcanada.ca/2026/07/fad-press-release-2026-07-15/ [7] Reuters — US producer prices post largest drop in 14 months; inflation risks still tilted to the upside — July 15, 2026 — https://www.reuters.com/business/us-producer-prices-unexpectedly-fall-june-2026-07-15/ [8] Reuters — Lower gasoline prices restrain US retail sales, underlying trend solid — July 16, 2026 — https://www.reuters.com/business/us-retail-sales-rise-marginally-june-2026-07-16/ [9] Reuters — ECB to hold rates now but energy price resurgence points to September hike: Reuters poll — July 16, 2026 — https://www.reuters.com/business/ecb-hold-rates-now-energy-price-resurgence-points-september-hike-2026-07-16/ [10] Reuters — US consumer sentiment improves in July; renewed Middle East conflict poses downside risk — July 17, 2026 — https://www.reuters.com/markets/europe/us-consumer-sentiment-improves-july-renewed-middle-east-conflict-poses-downside-2026-07-17/ [11] Reuters — US single-family housing starts, building permits fall in June — July 17, 2026 — https://www.reuters.com/world/us-single-family-housing-starts-building-permits-fall-june-2026-07-17/ [12] Reuters — South Korea central bank to raise rates for first time in over three years on July 16 — July 14, 2026 — https://www.reuters.com/world/asia-pacific/south-korea-central-bank-raise-rates-first-time-over-three-years-july-16-2026-07-14/ [13] StreetStats — U.S. Treasury Yield Curve — July 15, 2026 — https://streetstats.finance/rates/treasuries [14] Yahoo Finance — US Dollar Index (DX-Y.NYB) Charts, Data & News — July 17, 2026 — https://finance.yahoo.com/quote/DX-Y.NYB/ [15] ICE — Brent Crude Futures Pricing — July 16, 2026 — https://www.ice.com/products/219/brent-crude-futures/data [16] Fortune — Current price of gold: July 14, 2026 — July 14, 2026 — https://fortune.com/article/current-price-of-gold-07-14-2026/ [17] Fortune — Current price of silver as of Friday, July 17, 2026 — July 17, 2026 — https://fortune.com/article/current-price-of-silver-7-17-2026/ [18] Quoniam — Corporate bonds 2026: Yields, risks and realistic scenarios — July 13, 2026 — https://www.quoniam.com/en/article/corporate-bonds-2026/ [19] Reuters — Wall Street bank earnings surge, lifted by trading and investment banking — July 14, 2026 — https://www.reuters.com/legal/transactional/wall-street-bank-earnings-surge-lifted-by-trading-investment-banking-2026-07-14/ [20] Financial Synergies — Weekly Market Recap | July 17, 2026 — July 17, 2026 — https://www.finsyn.com/weekly-market-recap-july-17-2026/ [21] Global X ETFs — The Next Big Theme: July 2026 — July 16, 2026 — https://www.globalxetfs.com/articles/the-next-big-theme-july-2026 [22] Reuters — US weekly jobless claims fall; labor market remains stable — July 16, 2026 — https://www.reuters.com/world/us/us-weekly-jobless-claims-fall-labor-market-remains-stable-2026-07-16/ [23] Arc Research — Gold COT Report: July 10, 2026 — July 10, 2026 — https://www.getarcresearch.com/commodities/gold/cot/2026-07-10

Methodology & Notes

Data was compiled from publicly available financial news sources, central bank releases, and market data providers within the coverage window of July 11, 2026 00:00:00 EST through July 17, 2026 11:00:00 EST. Price ranges for precious metals and energy commodities are approximated based on available spot and front-month futures data during the period. The report includes scheduled economic data releases up to 11:00 AM EST on Friday, July 17, 2026, including the University of Michigan Consumer Sentiment preliminary reading (10:00 AM release) and U.S. Housing Starts (8:30 AM release). All price data is approximate and sourced from publicly available market data providers. Positioning data (COT) reflects the most recent available report as of the coverage period end. The report was generated on July 17, 2026 at 11:00 AM EST (Standard Edition).

Disclosure

This report is for informational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instrument. The views expressed are based on publicly available information believed to be reliable, but accuracy or completeness cannot be guaranteed. Past performance is not indicative of future results. Readers should conduct their own analysis and consult qualified professionals before making any financial decisions.

#WiseGold #PreciousMetals #Gold #Silver #MacroEconomics #MonetaryPolicy #Inflation #FederalReserve #GeopoliticalRisk #EnergyMarkets #Stagflation #WealthManagement #FinancialAdvisors #FamilyOffice #PortfolioStrategy #AlternativeAssets #WiseGoldCapital