When Ceasefire Breaks and Rates Hold: What the World’s Most Turbulent Week Tells Us About Gold, Risk, and the Road Ahead

WiseGold Weekly Pulse | July 10, 2026

Coverage Period: Jun 4, 2026 (00:00:00 EST) to Jul 10, 2026 (11:00:00 EST)

WiseGold Capital partners with advisors to assist them in managing assets for their clients. WiseGold Capital is not an asset manager or financial advisor; it is a consulting and logistics firm. Nothing in this publication constitutes investment advice.

About WiseGold

The WiseGold Weekly Pulse is published by WiseGold, a consulting and logistics firm that partners with financial advisors, family offices, and money managers to facilitate access to physical precious metals as part of a broader wealth preservation and portfolio diversification framework. Additional resources, including institutional-grade market commentary, educational content on precious metals fundamentals, and information on WiseGold’s advisory support services, are available at https://wise.gold.

Executive Summary

Global markets navigated a complex week characterized by escalating geopolitical tensions in the Middle East and mixed macroeconomic signals. The resumption of hostilities between the U.S. and Iran severely disrupted the fragile ceasefire, leading to a temporary halt in shipping through the Strait of Hormuz and a subsequent surge in oil prices [14] [15]. Concurrently, the release of the Federal Open Market Committee (FOMC) June minutes revealed a divided central bank grappling with persistent inflation concerns, dampening expectations for near-term rate cuts [1] [2]. In the Eurozone, the European Central Bank (ECB) maintained a cautious stance amidst signs of easing but still elevated inflation [3] [4]. The precious metals sector experienced volatility, with gold initially dipping on hawkish Fed sentiment before rebounding as safe-haven demand resurged following the geopolitical escalation [11] [12].

Key Takeaways

- U.S.-Iran conflict escalation disrupted the Strait of Hormuz, driving oil prices higher.

- FOMC minutes indicated a split committee with growing concerns over inflation persistence.

- U.S. labor market data showed signs of cooling, complicating the Fed’s policy outlook.

- Gold prices exhibited volatility, balancing hawkish rate expectations against safe-haven flows.

- Central bank gold purchases remained robust, providing structural support for bullion.

Market & Macro Week-in-Review Timeline

- Sat Jul 4: Initial Jobless Claims decreased to 215,000, suggesting a still resilient labor market [5].

- Mon Jul 6: U.S. ISM Services PMI registered 54.0%, indicating continued expansion but at a slower pace [9] [10].

- Tue Jul 7: U.S. median inflation expectations for one year ahead rose to 3.7%, the highest since September 2023 [6].

- Wed Jul 8: FOMC June minutes released, showing a divided committee on the future path of interest rates [1] [2].

- Thu Jul 9: U.S. and Iran traded fresh military strikes, effectively collapsing the recent ceasefire agreement [14] [15].

- Fri Jul 10 (10:00): Global equity markets faced downward pressure as geopolitical risks outweighed tech-driven optimism [7] [8].

Thematic Deep Dives

Macro & Monetary Policy

The monetary policy landscape was dominated by the release of the FOMC’s June meeting minutes. The document highlighted a clear division among policymakers. While some participants saw a scenario where inflation could ease, allowing for lower rates, “almost all” of the group concerned with persistent inflation considered a rate increase necessary if price pressures remained elevated [1] [2]. The debate underscored the Fed’s data-dependent approach and the diminishing likelihood of near-term rate cuts. Globally, the ECB maintained a cautious stance, acknowledging progress on inflation but remaining vigilant against secondary effects [3] [4].

Inflation & Growth Data

Inflation data presented a mixed picture. In the U.S., median inflation expectations for the year ahead rose to 3.7%, reflecting lingering consumer concerns [6]. However, the U.S. ISM Services PMI indicated continued economic expansion, albeit at a slightly slower pace, with the Prices Index decreasing to 67.7%, suggesting some easing in input cost pressures [9] [10]. In Europe, German CPI slowed to 2.3% in June, aligning with the ECB’s broader disinflationary narrative [4].

Rates & Yield Curve Dynamics

U.S. Treasury yields experienced upward pressure, driven by the hawkish tone of the FOMC minutes and the repricing of rate expectations. The 10-year Treasury yield climbed above 4.5%, reflecting concerns that the Fed may need to maintain higher rates for longer to combat stubborn inflation [8]. The yield curve remained inverted, signaling ongoing market apprehension about the medium-term economic outlook.

FX & Dollar Landscape

The U.S. Dollar Index (DXY) exhibited resilience, supported by the prospect of prolonged restrictive monetary policy. The dollar’s strength was particularly notable against the Japanese Yen, which weakened past the 162 mark, its softest level since the 1980s, despite resilient business sentiment in Japan [7]. The Euro remained relatively stable against the dollar, anchored by the ECB’s measured policy approach.

Energy & Broader Commodities Context

Energy markets were highly volatile, primarily driven by the renewed conflict between the U.S. and Iran. The escalation threatened shipping through the critical Strait of Hormuz, causing Brent crude to spike towards $79 per barrel [14] [15]. This geopolitical risk premium overshadowed the earlier downward pressure on prices stemming from concerns over global demand and the anticipated increase in OPEC+ production [13].

Precious Metals Focus

- Gold: Traded roughly $4,100 to $4,140/oz.

- Silver: Traded roughly $58.00 to $61.50/oz.

- Platinum: Traded roughly $1,610 to $1,780/oz.

- Palladium:Traded roughly $1,200 to $1,300/oz.

Precious metals experienced a tug-of-war between competing forces. Initially, gold prices dipped under the weight of hawkish Fed expectations and rising Treasury yields. However, the escalation in the Middle East reignited safe-haven demand, helping bullion recover some of its losses by the end of the week [11] [12]. Positioning data indicated a slight reduction in bullish bets among futures traders, while central bank demand, particularly from Poland and China, continued to provide a strong structural floor for prices [16] [17].

Credit & Liquidity

Credit markets remained relatively stable despite the geopolitical turbulence. Corporate bond spreads hovered near long-term averages, as investors continued to seek yield in a higher-for-longer environment. However, the resurgence of inflation concerns could prompt a reassessment of credit risk in the coming weeks.

Equity & Volatility Sentiment

Global equity markets faced headwinds as the week progressed. The initial optimism surrounding AI-driven tech stocks was overshadowed by the hawkish FOMC minutes and the escalating Middle East conflict [7] [8]. The CBOE Volatility Index (VIX) edged higher, reflecting increased market anxiety and a shift towards risk aversion.

Geopolitics & Strategic Risk

Geopolitical risk took center stage with the collapse of the U.S.-Iran ceasefire. The exchange of military strikes and the subsequent disruption to shipping in the Strait of Hormuz significantly elevated the threat of a broader regional conflict [14] [15]. This development has profound implications for global energy supplies and market stability.

Structural & Long-Term Themes

The ongoing structural shift towards multipolarity and the weaponization of trade and energy routes were starkly highlighted by the events in the Middle East. Central banks’ continued accumulation of gold reserves underscores a long-term trend of diversification away from the U.S. dollar, driven by geopolitical uncertainties and the desire for financial autonomy [16] [17].

Cross-Asset Interlinkages

- The hawkish tilt in the FOMC minutes drove U.S. Treasury yields higher, which initially exerted downward pressure on non-yielding assets like gold.

- The escalation of the U.S.-Iran conflict caused a spike in oil prices, reigniting inflation fears and complicating the central banks’ policy paths.

- The surge in geopolitical risk prompted a flight to safety, supporting the U.S. dollar and eventually leading to a rebound in gold prices.

- The combination of higher yields and geopolitical uncertainty weighed on global equity markets, leading to increased volatility.

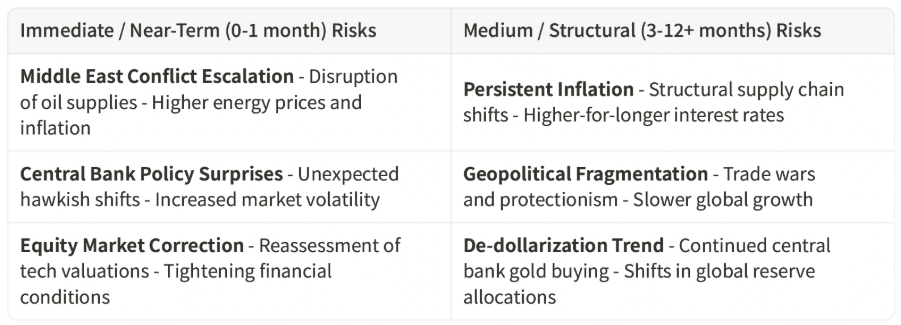

Risk Matrix Snapshot

Scenario Watch & Forward Catalysts

- U.S. CPI Data Release (Mid-July): Base Probability. A higher-than-expected print could solidify expectations for further Fed tightening, posing a headwind to precious metals.

- Further Escalation in the Middle East: Elevated Probability. Continued military strikes could severely disrupt oil supplies, driving energy prices higher and boosting safe-haven demand for gold.

- Resumption of U.S.-Iran Peace Talks: Low-Probability Tail. A sudden diplomatic breakthrough could reduce geopolitical risk premiums, potentially leading to a pullback in oil and gold prices.

Portfolio Context & Implications

The events of the past week underscore the importance of maintaining a diversified portfolio in the face of macroeconomic and geopolitical uncertainties. The resurgence of inflation concerns and the escalation of conflict in the Middle East highlight the potential vulnerabilities of traditional asset classes. In this context, assets that offer safe-haven characteristics and protection against purchasing power erosion may play a valuable role in enhancing portfolio resilience.

Precious Metals Strategic Thesis

Diversification Attribute

Precious metals, particularly gold, continue to demonstrate their value as a non-correlated asset class. During periods of heightened geopolitical stress and equity market volatility, gold’s performance often diverges from traditional financial assets, providing a stabilizing effect on portfolios.

Wealth Protection & Purchasing Power

The persistent nature of inflation, as evidenced by the recent uptick in energy prices and consumer expectations, reinforces the rationale for holding hard assets. Gold has historically served as a reliable store of value, protecting purchasing power against the erosive effects of fiat currency depreciation.

Drawdown Mitigation & Crisis Optionality

The sudden collapse of the U.S.-Iran ceasefire serves as a stark reminder of the unpredictability of geopolitical events. Gold’s status as a safe-haven asset provides investors with crisis optionality, offering a potential hedge against severe market drawdowns triggered by unforeseen shocks.

Structural Demand Drivers

The robust and sustained demand for gold from central banks, particularly in emerging markets, provides a strong structural foundation for the precious metals market [16] [17]. This trend reflects a broader strategic shift towards diversification and financial independence, which is likely to persist in the medium to long term.

Allocation Framing

From a strategic perspective, an allocation to precious metals is often viewed as a prudent measure to enhance portfolio robustness. While the optimal allocation varies depending on individual risk tolerance and investment objectives, the inclusion of gold and other precious metals can contribute to a more balanced and resilient investment strategy.

Summary Capsule

- Macro Pulse: U.S. inflation concerns persist, complicating the Fed’s policy outlook.

- Metals Stance: Gold remains supported by safe-haven flows and central bank demand despite hawkish rate expectations.

- Risk Tone: Geopolitical tensions have elevated market anxiety and volatility.

- Positioning Nuance: Futures traders slightly reduced bullish bets on gold, but structural demand remains strong.

- Forward Watch: Key focus on upcoming U.S. inflation data and developments in the Middle East.

- Structural Theme: Central bank gold accumulation underscores the ongoing trend of de-dollarization and diversification.

Source List

[1] CNBC — Fed officials were split on direction of interest rates at last meeting, minutes show — July 8, 2026 — https://www.cnbc.com/2026/07/08/fed-minutes-june-2026-.html [2] Reuters — Fed policymakers’ inflation concerns grew at June meeting, minutes show — July 8, 2026 — https://www.reuters.com/business/fed-minutes-due-analysts-debate-whether-warsh-will-curtail-them-2026-07-08/ [3] European Central Bank — Meeting of 10–11 June 2026 — July 9, 2026 — https://www.ecb.europa.eu/press/accounts/2026/html/ecb.mg260709~0e7f8241c9.en.html [4] State Street Global Advisors — US labor data raises fresh questions again — July 6, 2026 — https://www.ssga.com/insights/weekly-economic-perspectives-07-july-2026.html [5] Trading Economics — United States Initial Jobless Claims — July 10, 2026 — https://tradingeconomics.com/united-states/jobless-claims [6] Trading Economics — United States Consumer Inflation Expectations — July 7, 2026 — https://tradingeconomics.com/united-states/inflation-expectations [7] BlackRock Investment Institute — Weekly market commentary — July 6, 2026 — https://www.blackrock.com/corporate/insights/blackrock-investment-institute/publications/weekly-commentary [8] Sage Advisory Services — Fixed Income Outlook in Five Charts Let Income Do the Work — July 8, 2026 — https://www.sageadvisory.com/article/fixed-income-outlook-in-five-charts-let-income-do-the-work [9] Institute for Supply Management — Services PMI at 54%; June 2026 ISM Services PMI Report — July 6, 2026 — https://www.prnewswire.com/news-releases/services-pmi-at-54-june-2026-ism-services-pmi-report-302817275.html [10] Advisor Perspectives — ISM Services PMI: Continued Expansion in June — July 6, 2026 — https://www.advisorperspectives.com/dshort/updates/2026/07/06/ism-services-pmi-june-2026 [11] Kitco News — Gold and silver’s 2026 price lows are likely in, and a return to fundamentals will see renewed gains Sprott’s Hemke — July 7, 2026 — https://www.kitco.com/news/article/2026-07-07/gold-and-silvers-2026-price-lows-are-likely-and-return-fundamentals-will [12] RTTNews — Gold Headed For Weekly Loss As US-Iran Tensions Escalate — July 10, 2026 — https://www.rttnews.com/3666010/gold-headed-for-weekly-loss-as-us-iran-tensions-escalate.aspx [13] IEA — Oil Market Report July 2026 — July 10, 2026 — https://www.iea.org/reports/oil-market-report-july-2026 [14] AP News — Is an Iran deal over and war back on? A timeline of the conflict and talks — July 8, 2026 — https://apnews.com/article/iran-us-timeline-trump-hormuz-war-ceasefire-04da58cbae991183f8b52ef5bf615963 [15] Al Jazeera — US-Iran war: Will peace talks resume, and when? — July 10, 2026 — https://www.aljazeera.com/news/2026/7/10/us-iran-war-will-peace-talks-ever-resume-and-when [16] Bloomberg — Poland Bought 82 Tons of Gold This Year, Central Banker Says — July 9, 2026 — https://www.bloomberg.com/news/articles/2026-07-09/poland-bought-82-tons-of-gold-this-year-central-banker-says [17] Kitco News — Central banks boost gold reserves with net 41 tonnes purchased in May World Gold Council — July 3, 2026 — https://www.kitco.com/news/article/2026-07-03/central-banks-boost-gold-reserves-net-41-tonnes-purchased-may-world-gold

Pending Verification

Exact ETF flow tonnage for the coverage period.

Methodology & Notes

Data for this report was compiled from publicly available financial news sources, central bank publications, and market data providers. Price ranges for precious metals are approximations based on spot and front-month futures trading activity during the coverage period. The coverage period extends through Friday 11:00 AM EST to incorporate late-breaking developments and scheduled data releases.

Disclosure

This report is for informational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instrument. The views expressed are based on publicly available information believed to be reliable, but accuracy or completeness cannot be guaranteed. Past performance is not indicative of future results. Readers should conduct their own analysis and consult qualified professionals before making any financial decisions.

#WiseGold #Gold #PreciousMetals #MacroEconomics #Inflation #CentralBanks #GeopoliticalRisk #WealthManagement #PortfolioDiversification #HardAssets #FinancialAdvisors #FamilyOffice #WiseGoldCapital